"We continue to buy shares of what is a unique company. They are working on revenue lines that we have no idea about. And it feels good to know that these are for solving problems of the world, that is the core of the business. Stay young Alphabet. Stay young."

To market to market to buy a fat pig Short intro and market piece again I am afraid for those of you who love this segment. It is too busy on a company front. So, quick sticks, here is the look in. US stocks closed lower, off the best levels by quite some stretch. The nerds of NASDAQ lost two-thirds of a percent, the broader market S&P sank three-tenths of a percent, whilst the Dow Industrial was off half of that (0.16 percent). There is US GDP today, that should be exciting! Rate hikes looming, please get that done already. I am tired of hearing every day will they or won't they. Just get the one done and then wait and see.

Locally, stocks were mixed to lower. Same-same today, AB InBev results have been poorly received. I guess there will be many moving parts in there for 18 months or so, you will just have to roll with the punches if you are part of the new machine that sells around 3 out of every 10 beers across the globe. Just three days ago a driverless truck delivered Bud, the first commercial delivery sans the driver. Wow. The driverless truck is "Otto". 120 miles of driving, Otto is an Uber initiative. Awesome news for all! Except truck drivers.

Company corner

Alphabet reported numbers last evening, this was for their third quarter just passed. This is of course the business originally known as Google. This business is not even 20 years old, yet is synonymous with one of the biggest jumps that we have made as humanity, the internet. The internet is your online everything. You can buy almost anything you want, you can research almost anything you want. Provided of course your internet is not restricted, some poor souls still have their internet screened, or worse, no internet at all. That is another story entirely.

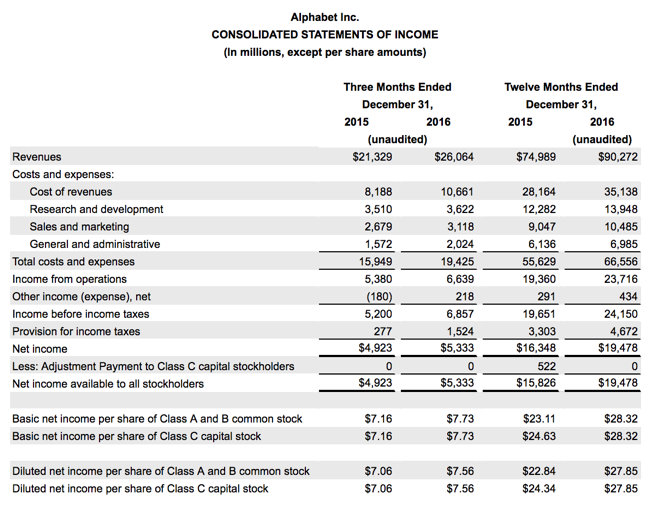

Quarterly revenues jumped 23 percent on a constant currency basis, 20 percent in Dollars to 22.451 billion Dollars. Take a moment to let that sink in, annual revenue approaching 100 billion Dollars and a business that has just become an "adult". GAAP operating income grew 26 percent to 5.767 billion Dollars, margins expanded and GAAP net income clocked just over 5 billion Dollars. On a per share basis, GAAP earnings per share clocked 7.25 Dollars. Non-GAAP, that number was 9.06 Dollars.

Whilst the business is called Alphabet, Google is still everything to the business, revenues from that "division" is 22.254 billion, the other segment, aptly named "other bets" generated quarterly revenues of 197 million Dollars and incurred losses of 865 million Dollars. What? Well, ruth Porat, the CFO credited with professionalizing the business at some level has done an extraordinary amount of work making the business more lean, more standard.

Her (Porat) Wall Street background has more than helped, she may have originated from the West coast (she was born in the UK actually), she spent nearly three decades across the country. The story goes about a time she was going to the gym (she likes spinning), she slipped on the icy curb and shattered her shoulder blade. Ouch. The surgeon said, we got to operate, she said, no can do, as CFO of Morgan Stanley, full year results were two days away. Sorry. No painkillers, that would make things fuzzy. So, off she went, delivered the results for the giant financial institution and only then went for the surgery. I am not too sure if that is dumb or valiant. Possibly both. Her father's entire family was killed in the holocaust, he hails from the Ukraine, ended up being a nuclear physicist. Being born in England, you could technically call her an immigrant, right? Sergey and Larry have an amazing person making the company leaner and more efficient.

Other bets, the moonshots, the dreams, the other businesses that potentially could change the world (and that suck a lot of cash right now) is a mixed bag. Calico is a healthcare business that focusses on longevity, on their website I find the "press" segment amusing: "As we make early progress on our research and goals, our capacity for handling press inquiries is limited. We'll do our best to be in touch". In other words, we are busy, leave us the hell alone. And then an explanation of what they are trying to achieve: "Calico's areas of interest are organized around understanding the basic biology of aging as well as interventions for serious age-related diseases. Calico is exploring the genetics of aging in human populations as well as in a variety of model organisms from yeast to worms to naked mole rats." Nice. So potentially this could be a very important business to Alphabet in the long run.

Another business is "The moonshot factory", which comes with an operating model. Simply called X, the business is designed to turn ideas into real technology. Technology that will change lives and make the world a better place. You may well argue that is the core of Google, the starting point.

And whilst the cash burn is huge for investors, the great ideas turned to prototypes, turned to awesome businesses, turned to bottom line expansion is something that takes a decade. Or more. Foghorn, which is carbon neutral fuel made from seawater sounds like something from a comic book, invented by Professor XYZ. Smart contact lenses, helping people with diabetes. The UK born Astro Teller (real name Eric Teller) runs the business, nicknamed Astro not for his love of small candy balls or science geekiness, rather a hairstyle that looked like fake grass. He looks amazing. Title for Astro? Captain of Moonshots. Ha ha!!

Google Ventures, now known as GV is part of other bets. Other bets that include startups with capital and expertise. This is where investments in Uber (you may recognize this business) and of course Nest, which is wholly owned. Google Ventures invested (Michael tells me) 258 million Dollars in Uber, giving them a 6.8 percent stake in 2013. Dilution along the way? Who knows, time will tell, recent reports suggest they still own the same percentage, it is possible they may have been diluted to half that. Uber is "worth" in the last fundraising, around 66 billion Dollars (June this year), if GV owns three and a half percent, then this is worth 2.31 billion Dollars. Or 0.42 percent of the entire parent company market cap. Ha-Ha! GV may become a more important business in time, as the company looks for other avenues to invest their resources.

Resources that last were 83.056 billion Dollars (Cash, cash equivalents, and marketable securities) at the end of the last quarter. And over 10 billion Dollars more than a year ago. Cash represents 15 percent of the current Alphabet market cap (nearly 550 billion Dollars). So whilst cash conservation and cost controls have been introduced by Ruth Porat, these other bets burn around 3.5 billion Dollars a year. As a shareholder you have to say, yes, this is actually worth every cent. In identifying the next big thing, thinking has always been encouraged at Alphabet slash Google.

We continue to buy shares of what is a unique company. They are working on revenue lines that we have no idea about. And it feels good to know that these are for solving problems of the world, that is the core of the business. Stay young Alphabet. Stay young.

Amazon reported numbers for the third quarter last evening. It is still very important to remember that Amazon is building a business. They are a long way from being mature, I am not too sure where that is, as long as the vision exists and Jeff Bezos has the energy to want to change the world. Like the aforementioned Alphabet, the vision of creating something amazing and huge keeps this business at the forefront of technological innovations. Getting stuff to your front door that you ordered an hour ago is pretty mind blowing. In the old days it took an hour to turn your computer on and to connect to the internet. Not quite, you know what I mean though, that sound where your telephone line connected at the exchange and the "handshake" sound it made, tinny and all. How times change.

And in large part, improving technologies has meant that Amazon have been able to expand other businesses. Amazon Web Services (AWS) increased sales by 55 percent year-on-year, to 3.231 billion Dollars for the last quarter. Operating income for that division increased to 861 million Dollars, up 101 percent year-on-year when measured against the corresponding quarter. For those of you who don't know what it is, AWS is cloud computing. i.e. You can host your website from anywhere and upload all your documents to the cloud.

All the "stuff" that used to be done physically at your desktop can now be done from anywhere, provided you have an internet connection. No more need to store vast documents locally. This business is only 10 years old, and is fast becoming an integral part of their business, representing 8.7 percent of total sales. If you are looking for all their products, visit the link above and then follow the products links. They are selling stuff (products) there that you have never heard of.

The business is still pretty much a US based business, 58.6 percent of the sales still come from that region, 32.7 percent is "international". Rolling twelve month sales clocked 128 billion (nearly) Dollars, up 27 percent year on year. Make no mistake, this business is growing off a bigger and bigger base all of the time. The disappointment however was that profits for the quarter fell and missed expectations, net income for the quarter was 252 million Dollars, this followed a blow out quarter prior to this period.

They continue to make a big loss in the international part of their business, so whilst sales increased 28 percent to 10.6 billion Dollars (for the quarter), the operating loss widened to 541 million Dollars. Twelve month sales for that segment was 41.9 billion Dollars, a huge number. For comparisons sake, Amazon North America registered sales of 75 billion Dollars for the rolling twelve months (i.e. the last four quarters). Home Depot has annual revenues of 88.5 billion Dollars. By this time next year, Amazon North America should have sales in excess of Home Depot. Only Costco and Walmart in North America will have bigger sales than Amazon. Amazon North America is now bigger than Target. Stick that in your tech pipe and smoke it.

Amazon is a business that has many irons in the fire, not too dissimilar to Alphabet. Just read through the Press Release - Amazon.com Announces Third Quarter Sales up 29% to $32.7 Billion. Content, Prime members getting movies, music, the Alexa software (Echo ecosystem) integrates with everything.

You get what you get with Amazon. This is a business that will invest heavily in their infrastructure leading to scant profitability. It won't always work, there will be lines that will be shut down. The user experience is what matters. Fourth quarter guidance may have disappointed some folks and been at the bottom end of the guidance. They had a laughable operating income guidance - "expected to be between $0 and $1.25 billion." Ha ha, that means that they could make nothing or they could make more than ten percent more than a record quarter.

This unsettles people into believing the long term story, they want steady profits now and an amazing future. As a result of unlimited resources, you cannot have it all. And hence you have to roll with the volatility in the share price, which is down five percent pre-market. Buy this business and own it, own it for a decade plus. By that stage it may well be challenging Walmart for the biggest retailer in North America. Or before. And you can bet that they will have many other interesting businesses along the way. Stay long, stay strong.

Linkfest, lap it up

Every week there is that one article that is a must read. Here is this weeks. It was so good that it was shared on our office WhatsApp group twice in 12 hours - Start Now. Time is your friend when it comes to investing, especially when the market has been flat like the last 18 months.

Beer and self driving trucks, sounds like a great combo! (Otto and Budweiser: First Shipment by Self-Driving Truck). Next step is beer being delivered by drones.

As the price of something drops, people use more of it. On shore wind generation costs have dropped by 30% over the last 5 years and solar costs have dropped by 66% - Renewables overtake coal as world's largest source of power capacity. Given how long it takes to build coal and nuclear power stations, I wonder if a Nuclear power plant starting tomorrow makes sense. If by the time it was completed the cost per megawatt would still be less than solar then maybe? Or would solar costs have dropped so much over the years of build time that solar power is cheaper than nuclear.

Home again, home again, jiggety-jog. There were multiple results overnight and over the last few days that we will get to. Amgen had results, we will get to those for sure! Apple have released new MacBooks, that is incredibly exciting. If you think about it, people drive expensive German Sedans for an hour or two a day and then sit in front of their scooter type performance at their desk. For ten odd hours a day. get your company to buy you a MacBook, tell them that IBM research has shown that you will be more productive and cost less over the life of the computer. Stocks are mixed across Asia.

Sent to you by Sasha, Byron and Michael on behalf of team Vestact.

Email us

Follow Sasha, Michael, Byron, Bright and Paul on Twitter

078 533 1063