To market, to market to buy a fat pig. It is not often that this happens, when you get a day that the bourse (when we close) basically registers a flat line. Well, not exactly, five and one quarter points better, or 0.01 percent. Unfortunately the gold miners sold off, nearly one and two thirds of a percent. The wage negotiations between the industry and the unions are ongoing, the gold miners put their best foot forward and offered a four percent wage increase and a benefit increase too, but it is literally a universe apart from what was put forward by some unions. NUM said this was an insult. More on the gold miners in a second!!

Over in Europe markets were pretty decent, the French were celebrating Bastille Day (the roll over to Monday from Sunday) and again the visuals from Europe's second biggest economy suggested that they were not finished. No potholes. No people in rags on the side of the road. No buildings going to ruin. Rather some pretty good looking aged buildings in the beautiful countryside. A lovely advert for France each and every year, the Tour de France, the 100th such event. On the other side of the Atlantic, stocks ended the day better than where they started, despite worse than anticipated retail sales. Check: A Slower Rate Of Growth For Retail Sales In June, But The Annual Pace Rises.

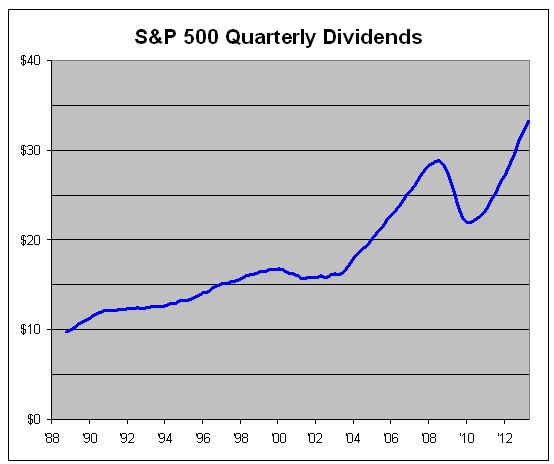

But hey, I stumbled across this piece: Irrational Exuberance Again? (excerpt), which suggests that based on collective S&P 500 earnings of 117.3 Dollars for 2014, the forward multiple is just a little over 14.3 times. Hardly expensive, it was maybe just too cheap at the beginning of the year. Another closing high for the S&P 500 tells you that this is the case, the collective think so too. 8 in a row!

As expected, we are going to start to see some of the trading updates of the Anglo stable companies, this first one was from Amplats yesterday. The release says that "Headline earnings per share ("HEPS") for the period is expected to increase to between 480 cents and 535 cents from 273 cents reported for the six months ended 30 June 2012." Sounds a lot better. Due to what? Well, the weaker Rand did benefit them, but there were also higher sales volumes which sounds encouraging. Results expected Monday next week. We will do a detailed write up then.

An ex Anglo company that still shares the name to some extent, but not the shareholder, AngloGold Ashanti announced yesterday alongside their results that they would look to "sharpen (their) focus on efficiency and to tighten up on costs, overheads and capital." And what that means is lower production guidance for the year, but pleasing to note that cash costs are in-line with expectations. Lower yield mines would attract less capital expenditure, that would be deferred to their higher quality production. Next quarterly results when we can expect more information is the 7th of August.

Byron beats the streets

On Friday Naspers announced a successful bond issuance of some significance. They managed to raise $750m 6% notes due by 2020. This compared to a similar raising done by the company in 2010 of $700m at 6.375%. A lot has changed since then, the company has grown a lot but interest rates have also increased significantly in recent weeks, especially for emerging markets. According to Bloomberg this is Africa's first overseas corporate bond sale in two months following a massive pullback on emerging market funding. You see how quickly money can talk.

What I find interesting is the sheer size and scale of the bond raising. $750m or R7.5bn is equivalent to the annual profits made from the paid TV business. The cash from that business is what they usually use to fund acquisitions. According to the balance sheet of their latest results, cash and cash equivalents sits at R15.8bn. Balance sheet gearing only sits at 12% so there is plenty room to raise some cash and probably why they got such a competitive rate.

But why are they raising this money? Here is what the announcement had to say: "The net proceeds will be used for general corporate purposes, including future acquisitions and the repayment of certain amounts outstanding under the Naspers group's revolving credit facilities."

It is pretty vague. Companies roll over debt because they feel their cash reserves can be put into better use elsewhere. This means that Naspers have lots of opportunities in the pipeline and as a shareholder this is good news. The company is taking advantage of the low interest environment so that they can grasp any opportunity that presents itself with both hands.

And we are well aware that the company is acquiring with a big focus on ecommerce in developing markets. It is certainly the way of the future. People are busier than ever before. Shopping online saves you time and money. Just the thought of having to park at Sandton City makes shopping online worth every cent. I am sure that parking in Turkey or India is even worse. It is simple and efficient and once people develop trust in the system, I think it will fly. Anyways who are we, or anyone else to question what Koos Bekker thinks the future of technology will be.

As big holders of the stock we welcome this news and wait with anticipation to hear what and where the next acquisition will be.

Jules Verne.

It has been exactly a year yesterday since GANGNAM STYLE was released by PSY. As I was doing this piece, the video had 1,743,631,346 hits. The most watched YouTube video of all time is not in English (the most spoken first and second language worldwide), it is not mandarin, which is the world's largest first language at roughly 12.5 percent of the globes population. But rather Gangnam style is in a language that is spoken by only 76 million people (as a first language), 1.14 percent of the globes population. And you can bet that the vast majority of the 24.5 million people in North Korea have not seen the YouTube clip, because of the oppressive regime that means a lack of internet connectivity. And an oppressive regime, oh, we said that. I bet that the folks would rather have freedom than the internet.

Google bought YouTube in late 2006 for 1.65 billion Dollars, not long after the company was founded on Valentines day in 2005. I went onto the YouTube website to get an idea of views/hits/uploads. Amazing, check it out: Statistics. The factoid that blew me away was: "Over 6 billion hours of video are watched each month on YouTube, that's almost an hour for every person on Earth, and 50% more than last year" More interesting is that in the Google first quarter results there is not a single mention of the word YouTube. Because it probably still costs them a lot (a huge amount) and probably does not make them that much. Yet. Results on the 18th of July, two days time. I can tell you that I am pumped for them!!

Staying with that theme of search, interwebs, download the Rimm-Kaufman Group Digital Marketing Report for the second quarter. You probably will have to give them a little information, but hey, who is anonymous anymore? Want that? Move to the Mosquito coast!! I have no idea why that bigot had such an impact on me in that book. Some interesting "stuff" in there.

"Stuff" that I picked out: "In Q2, 58% of visits from social sites were generated by Facebook." AND, this takes a couple of reads to sink in: "Although the iPad saw its share of tablet traffic slip from Q4 to Q1, it has held steady since then, generating 85% of tablet clicks." And then lastly: "Google commanded 80% of search spend and 81% of search clicks in Q2 as Bing Ads continued to chip away at both metrics." Bing, too little too late? I see that Microsoft is rated a sell by a couple of investment houses whilst Apple, Google and Facebook are mostly buys. All fun.....

In recent months I have been hearing this theory. And it was bound to happen. After 15 years of higher than anticipated oil prices the price has levelled off over the last half a decade. Here was an interesting article from the BuzzFeed business segment: Here's Why "Peak Oil" Peaked. Peak supply is what everyone is talking about. And the reason why is that humans are becoming far more efficient than ever before. True story. I am however the furthest thing from a petrolhead. I have watched maybe two whole episodes of Top Gear in my life. A motor vehicle gets me from home to work and back. And all the other driving in-between. Free piston Stirling engine, bring it on!! But to get to the core of that argument, is this peak oil production? Will efficiencies trump longer term demand, because of the price of a barrel of oil? Possibly. Time will tell.

This is not a widely held view, but it should be: Wal-Mart deserves the 2013 Nobel peace prize for improving the lives of millions of low-income consumers globally. OK, perhaps not the Nobel peace prize, I would give that to "the internet" if there was such a recipient. But lower prices equals more spending power and lower inflation, which translates to higher standards of living. Labour might view the company as exploitive, but without the business consumers (the majority of us) would be all the poorer, both literally and figuratively. The largest company by sales globally, but not the most valuable, that tells you that retail is a tough old trade!!!

Home again, home again, jiggety-jog. Sis. European motor vehicle sales released this morning are terrible. Signs were there a couple of months ago that we had bottomed. False bottom? What does that even mean? No bottoms today, stocks are lower to start with!

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440