To market, to market to buy a fat pig. Stocks rocked again here in Jozi, the gold miners had an absolute pearler of a day, a peach of a day, GoldFields and Harmony up over seven percent apiece. Some said the Rand, which weakened to a four year low during the session intraday could have something to do with it. Some said that it was a technical bounce. I thought that the stories around the silicosis lawsuit being directed elsewhere was one reason, and the finalisation of a deal to buy old South African gold assets could be the other reason. Some expecting a jump in the gold price soon after all the recent selling, some suggesting fund flows from the gold equity bulls. All I know is that Harmony Gold is down nearly 61 percent since mid October 2002. GLD, the Rand Gold price instrument, that allows you to hold the physical gold as an instrument, listed in November 2004. Since then, it is up 431 percent. Yowsers. GoldFields over the same time frame is down over 25 percent, it doesn't really matter if you add back the Sibanye Gold, the All Share Index over the same time period is up 325 percent. In Rand terms.

Back then in October 2002 the Rand was at 10.40 odd to the US Dollar. The low, lows was late 2004, 5.65 to the US Dollar. In the post Lehman Brothers collapse and depths of despair in the storm that was the great financial crisis, the Rand weakened to beyond 11.10 to the US dollar. The subsequent recovery saw the Rand firm to 6.60 to the US dollar in late April of 2011. And now we are back at 9.10 and beyond. Honestly, how do you plan in that kind of environment as an importer or exporter? The Euro has been less volatile, but around about the same story. That is what the free market gives you, volatility. And unless you are a major currency, the headwinds batter you more. The Indian Rupee is 26 percent weaker over 5 years, the Brazilian Real is 14.5 percent weaker, strangely, we are a less 11.38 percent weaker from the same point. So, don't get anxious, it is a lot about the US economic health improving substantially and want for Dollar based assets again.

Bill McBride over at Calculated Risk sheds some insight: Fed's Q4 Flow of Funds: Household Mortgage Debt down $1.2 Trillion from Peak. Deleveraging has taken place. He suggests it is not over, but heading in the right direction. What is more important, and Byron alluded to it a while back, the "feeling rich" factor. The WSJ fleshes that out: Freshly Flush, the Consumer Is Back. Minus debts and liabilities, the net worth of American households in the last quarter was 66.07 trillion Dollars. And bear in mind that we have had a serious rally in the first quarter of this year, as well as a housing market that continues to improve. So I expect when the Federal Reserve releases that same report in early June (when the days are shorter and colder here) the overall wealth will be much higher. And you know what people do when they feel richer? They spend. The Americans are good at spending, it makes their economy go around. That should be good for all of us.

Mark Perry had another set of graphs: Rising stock market and housing recovery bring US household net worth above pre-recession level. I have taken the one from his piece that I think is most important. 66 trillion. In 2002 that number was barely

Quickly back to the Jozi markets, stocks were obviously buoyed by a 6.9 percent move northwards in the gold sector, platinum miners actually sank 0.16 percent. Wow. Resource stocks collectively added 1.6 percent plus, sending the market to its best levels since mid February. The high, highs were from earlier in Feb, with the All Share intraday a whisker away from 41 thousand points. We are currently at and around 40720 points. Another couple of good days for us here locally and we will be through those recent all time highs. I suppose a good non-farm payrolls number might actually see another rally higher. We don't have to wait long, around three thirty local time here to see that number. This might give the commodities complex a bit of a lift today: China Export Surge Helps New Leaders Sustain Rebound: Economy. Still, I wonder when we are going to see the real impact of the Chinese consumer, when are they going to be driving consumption.

Over on Wall Street the Dow Industrials closed at another record high, the S&P 500 was still creeping up getting closer to the all time high, but around 20 odd points to go so still over a percent and one third away. But, as I said above, it is all about the jobs number today. The expectation is around 165 thousand jobs, the impact of the sequester on the government employment in the US, that is a big issue in the coming months. For now though, everything looks like the same as last month. I am interested to see whether or not there will be revisions to the prior months, that would indicate that the labour market continues to improve. The weekly jobless claims have moved down by around 6-8 percent over the last few months, that could have quite a big and long lasting impact. Now that Americans are richer, perhaps that will lead to greater job creation.

Oh, but whilst the Dow Jones managed to reach another all time high, Cullen Roche points this out: Pessimism Rises Even as Dow Hits a New High. As you can see, the bearish sentiment is around 30 percent higher than "the usual" bearishness. But what seems strange is that the neutral view is changing to both bullish and bearish. I get that. People get off the fence, which is a good thing.

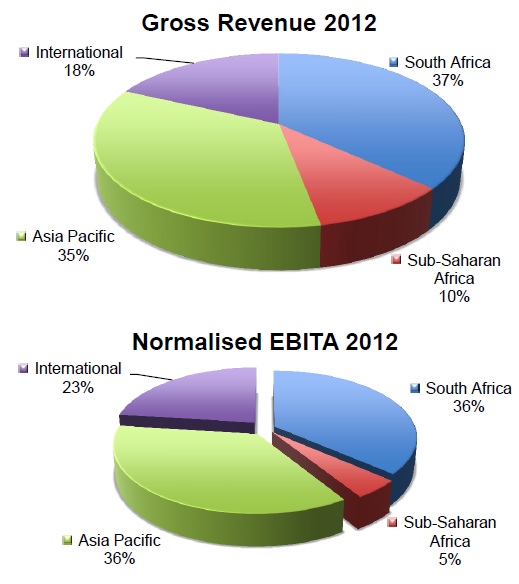

Ok, one of the most important stocks in the Vestact stable, Aspen Pharma reported numbers for the half year to end December. Revenues from continuing operations increased 20 percent to 9 billion Rands, operating profits increased by 24 percent to 2.5 billion Rands. This translated to normalised diluted headline earnings per share of 379 cents. Cash generated from operating activities grew 9 percent to 1.3 billion Rands. Gross profits grew 22 percent to 4.3 billion ZAR. Profits before tax grew by 29 percent.

Ok, that was all the important numbers, the segmental revenue and profits view give you a pretty good idea that Aspen is no longer a South African company. 63 percent of revenue and 64 percent of EBITA comes from outside of our borders. Byron suggested on the box this morning that if the company did not have that sort of exposure the stock price from the South African earnings alone could be 110 odd Rands a share lower. I suspect it might even be more, the reason why Aspen commands a much higher rating relative to the rest of the market is that they have managed to grow aggressively. And that Asia Pacific springboard is wound tight in Australia, they have a twenty percent market share there in scripts written. See the numbers below, from the Segmental contribution for six months ended December, slide 17.

The great thing about their two major businesses, SA Pharma and Asia Pacific is that they both managed to grow revenues in excess of 20 percent. Margins have actually improved over the last two years, with group operating margin having increased 30 basis points from the prior comparative period. Just to give you an indication of how quickly this company is growing, revenue for this half is double what it was for the half four years ago. More than double in fact.

In their local business, the South African one, the core business had a good first half, the baby formula business did well. The ARV's business is expected to slow, you can imagine the margins are not that great. In the second half Aspen continue to expect the baby formula business to do well. I remember those days of baby formula, when you couldn't go anywhere without a couple of feeds. Those were the days my friends, they did end and the sleep sort of started. The next business division, the Asia Pacific business is where the real growth is going to come from. The move to use Australia as a springboard and to buy Sigma. I remember there were many naysayers back then, they were overpaying, remember? 6.1 billion Rands back then. I suspect that whilst that will capture the attention of the analyst community, the opening of a company on the ground in Nigeria is also exciting.

The reasons that I say that is because you must look at the territories that the company operates in and then this table, sort by healthcare spend to GDP, data from the World Bank: Health expenditure, total (% of GDP). At the top of the pile, if you order descending, the US is miles ahead of the major European economies, spending 18 odd percent on healthcare relative to GDP. Phew. Lower down, you have France at 11.9 percent, Germany at 11.6 percent, the Netherlands at 11.9 percent, that is seemingly the number. Ten to 15 years on however, because the data is supplied from the 1998 period onwards, those developed countries are spending 100 basis points more on healthcare than they used to. And although economic growth rates have been slow, the spend on healthcare continues to rise in rich countries.

Now, I am getting more to the point for Aspen. Let us look at Asia, the Philippines, Indonesia, Thailand, China and Vietnam, what is their spend as a percentage of their relative GDP? The Philippines, it is 3.6 percent. In Indonesia it is 2.6 percent. In Vietnam it is slightly higher at 6.8 percent, Thailand is 3.9 percent whilst in China, where the population is around 1.35 billion folks, it is not on this list, but a Bloomberg story (China Health-Care Spending May Hit $1 Trillion by 2020) suggests that it is around 5.5 percent, but could grow to 7 percent of GDP by the year 2020. The suggestion is that it would treble in the next seven years. Wow. And that is the point that is worth making, whilst richer countries continue to pay more for healthcare off a higher base, the real potential is in markets where medical spend is still low, but growing fast. And Aspen is well positioned in these markets, especially Asia and locally across our continent. I saw a report this morning on agriculture that predicted that by 2050, 81 percent of the worlds population will be in these regions. All needing better healthcare than they did before.

Valuations are really stretched, the stock has been on an absolute tear lately. The stock is up around 90 Rands from around 106 ZAR a year ago. Five years ago it was 30 odd ZAR. The increase in the share price has been meteoric. If the company makes a little less than 8 Rands for the full year to end September, the stock will trade on a 25 multiple at current price levels. Earnings however continue to grow at a really healthy click though, a 15 to 20 percent earnings growth rate should be the norm for the next two years. Driving the share price has been North American buyers, look at slide 28 on that same presentation, Distribution of fund managers. It is South Africans and Europeans that think the stock is expensive, because they are fewer.

Add to the potential of their Asian business to their robust and equally fast growing Latin America and African businesses and you can quickly see the reasons why investors are paying up for this stock. We continue to hold and add where we see fit, this is a decade long investment at least.

Byron beats the streets. Yesterday we received very good looking results for the 6 month period ended 31 December 2012 from Spur Corporation. Revenue increased 40.4% to R336 million on the back of good loyalty programmes, promotions and a very strong Christmas period. This equated to a 33.1% increase in headline earnings to R77.4 million. This equated to 90c per share. The second period is usually weaker than the first because it does not include Christmas but because the company is growing fast lets annualise this number. At R1.80 earnings for the year and the stock trading at R27.65 it affords a P/E ratio of 15 which is reasonable. The stock has had a fantastic run of late trading at half this price at the end of 2011.

Sales across the group grew 17.5%. Spur sales were up 16.5%, Panarottis sales were up 30.6% and John Dory's grew sales 11%. The biggest revenue driver however was from manufacturing and distribution which rose 85.7% following the integration of the DoRego's distribution centre which is turning out to be a good purchase. The international business also had a good turnaround growing sales by 26.4% after actually bucking the trend in the UK.

All in all a very good set of numbers. The company now compromises 471 restaurants up from 456 six months ago. They plan to open up 11 new Spurs, 1 Panarottis and two DoRegos in the next 6 months and are planning second Spurs in Tanzania, Nigeria and Swaziland. I am also very impressed by their innovative drive with loyalty programmes and promotions which have clearly been a success. Their adverts have been all over the place, both Spur and Panarottis, as irritating as they may be, they are creating awareness.

I also like the sector. The industry is going to grow fast in developing countries. Eating out is a luxury and people aspire to be able to afford that. Demographics are also changing as people work harder and longer hours and just don't feel like cooking after a long hard day. Rather go and relax in a happy environment like Spur with good value for money food.

I still prefer the Famous Brands mix and with that extra fast food element, the franchisee input costs are less and therefore it is easier to grow the number of Restaurants. Most of Spurs business involves the sit down and serve model. But having said that, Spur looks cheaper and is coming off a lower base.

Crow's nest. At Lake Como in Italy they have a wonderful get together behind closed doors every year. The location is stunning. So whilst bureaucracy continues to be the glue that keeps Italy together, Italian politics is in disarray. As usual. It is in a constant state of crisis, with a massive gap in the last decade or so. Silvio Berlusconi has three separate charges against him, just yesterday a court in Milan convicted Berlusconni to one year in jail for breach of confidentiality, but strangely the court issued no orders to carry out the sentence. The more things change ..... and you think that we have problems politically here? Well, Jim O'Neill and Nouriel Roubini were interviewed, Jim gave a sunny outlook whilst Nouriel was always bearish. Sigh. No credibility, I got mad and shouted at the screen, the word fraud even came up. Telling us that things are always so bad. If he is so convinced he should short all asset classes and make a bomb. I notice that one of his lieutenants, Megan Greene left and started her own thing. Yeah, the droning got too much for her too. Anyhows, jobs, jobs and more jobs today, the biggest event in our world, even if we "do nothing" around it, it is fun to watch.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment