Jozi, Jozi 26o 12' 16" S, 28o 2' 44" E. Phew. It has still been a time of reflection on the events of last week, we saw our parliamentarians on both sides of the aisle exhibiting politicking of the highest order, enough to make one weep and laugh at the same time. And not once did anyone say, ok, we are all to blame here. Civil society, government, the unions, the company, the community, all of us for breaking promises, not keeping the peace (being too violent at the same time) and not speeding up reforms of all sorts. Reforms from all people. There have been many articles written about the massacre, the events leading to it, the aftermath and the blame game. There is no simple answer, nor should you only have one point of view. It is too easy to have an answer, the practical middle ground one about business. Too easy. Still, I would like to hear your point of view.

Ye olde worlde. The rumours around the ECB, the Bundesbank, ECB sovereign debt buying of peripheral debt continued to do the rounds, with a are-they-or-are-they-not? And they are the ECB, because the European Central Bank has indicated that this is something that they would like to do, to lower the spreads on the short term government debt. You don't need to understand the nitty gritty, just understand that the intention is for the peripheral countries in the Euro Zone, most notably Spain and Italy to have access to cheaper short term funding. The thinking is that when "things" settle and investors are not so skittish, then the longer dated issuances will become a reality at lower yields. I can appreciate that a lot of it is around sentiment, the reality is not going to change immediately. These events are going to impact on our markets in the very short-term, we still maintain that the Europeans are going to get the job done. They are definitely on it. And although the outsiders are spouting their pearls of wisdom on what the Europeans should, or should not do, we are comfortable that all hands on are deck.

OK, so we have perhaps one of the most important days today, well at least for us over at Vestact here. No, it is not the fact that we have the sliding doors open celebrating the arrival of spring, but rather the fact that BHP Billiton reported their full year numbers this morning. Byron was so excited he did not sleep last night. No, that is not entirely true, he slept well he told me, but the excitement around the results are of course high here in our office. Market nerds.

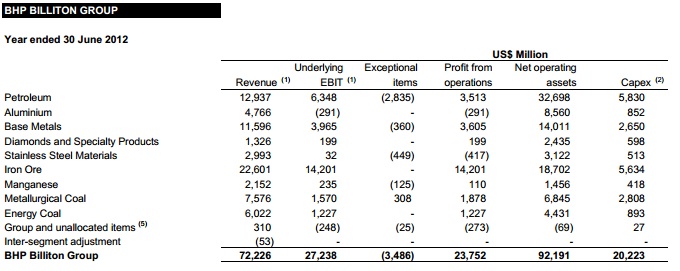

Time to dive straight in, the full release is available for download here Report for the year ended 30 June 2012. Revenue up ever so marginally to 72.226 billion Dollars, net profits off 34.8 percent to 15.417 billion Dollars. Phew, that is a big number, but markedly lower than this time last year, when the number clocked 23.6 billion Dollars. Gearing is now 26 percent, this has not changed that much. Underlying EBIT registered a 14.8 percent fall to 27.238 billion Dollars, profit from operations fell to 23.752 billion Dollars, there were some exceptional items which we deal with below. Here is an operational overview, which I hacked from the results release:

Why the big fall in profits? Well, there were a number of telegraphed write downs, including gas assets bought from Chesapeake, remember we wrote about this on the third of August: BHP Billiton write offs. There was of course also the Nickel West impairment, and a charge taken at Olympic Dam. We will deal with Olympic Dam a little later in more detail, it is important in these numbers. All in all exceptional items nearly topped 2.5 billion Dollars, or 3.7 billion Dollars before tax. It is a whopper. Also impacting on earnings were the weaker commodity markets and rising costs, it is not just a South African issue that. BHP Billiton have dealt with the costs issues by closing several production facilities, two down under and one here in South Africa. Controlling costs is harder when you have fewer operations, that is for sure, when you have smaller ones, such as these ones that have been shut it is easier!

The final dividend is a little higher than last year, now at 57 US cents per share. At the current exchange rate, of around 8.27 to the US Dollar, that translates to around 471 ZA cents for the second half. This follows a dividend payment of 55 US cents, actual payment of 418.96 ZA cents per share at the half year stage. No exchange rate announced for the Rand dividend yet, expect that announcement in around three weeks time. But, if the exchange rate were to remain the same, the Rand payment would be 890 ZA cents for the year. At the closing share price of 257.2 Rands last evening, the company is yielding 3.46 percent. I guess that is more than acceptable for the risk that you assume as a shareholder of the very biggest mining company on the planet. Basic earnings per share after exceptional items showed a 32.5 percent drop to 289.5 US cents per share. Roughly that translates to 2395 ZA cents per share. Again, at a 257.2 ZAR closing price, the company trades on a historic multiple of 10.74 times earnings. That is hardly expensive, but the market has got the share price levels relative to the news flow correct. Well done Mr. Market.

At ten of their operations BHP Billiton achieved record production. We covered their production report when it was released in mid July: BHP Billiton production report for Q4. But here is perhaps the biggest disappointment, but NOT something unexpected, the uncertainty around the development of Olympic Dam continues. Delays. For those of you who do not know what Olympic Dam is, the company has a pretty good explanation: "Olympic Dam is a multi-mineral ore body containing uranium oxide, copper, gold and silver. Olympic Dam is Australia's largest underground mine." Kloppers made a good comment, you will recall that nuclear energy was all the rage and there was much excitement about that, until the Japanese disaster at Fukushima Daiichi. His comment was that the landscape had changed, and therefore the development of Olympic Dam is not going to be what investors had expected. Also, the costs in Australia have risen quite sharply and therefore BHP Billiton are looking at cheaper ways of developing this one of a kind asset. The company therefore says that there is a "change in status" of the project.

So, now that shareholders are expecting lower capex as a result of iffy demand and a less uncertain outlook, how is the company going to allocate capital. "first: invest in high return growth opportunities throughout the economic cycle" And this means projects like the Jansen Potash mine will be prioritised above all else. At the moment. Of course the company invested heavily in the period of the financial crisis, when everyone else was stationary. The company is at pains to point this out, as the differential from their peer group. "second: maintain a solid A credit rating" This means that the level of gearing should be maintained at current levels, and when the company raises money for expansion, they are acutely aware of balance sheet relative strength.

In the presentation the capital allocation continues: "third: grow our progressive dividend" This of course is good news for shareholders, who have been patient. "fourth: return excess capital to shareholders" There were no buybacks in the last financial year, following the whopper in 2011, around 10 billion Dollars. Expect that to happen at some stage in the future, for us South Africans it might not be the most effective way of returning capital to shareholders, but in some other places where the company is listed, most notably Australia, this makes sense. You can't please all of your shareholders when they invest in multiple geographies with different jurisdictions.

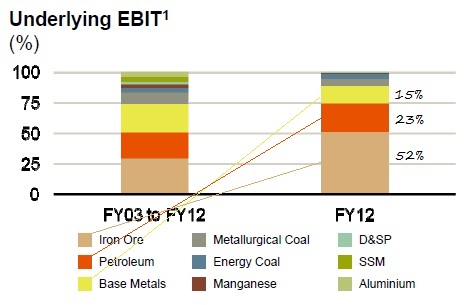

Before I end off, with both their conclusion and our own, I think that it is important to note the earnings mix. It is still for most intents and purposes a three division business. Check out this hacked piece from a slide in their presentation, I have written their underlying EBIT contribution relative to the overall number:

Iron Ore is still the champion, but less so than before. The petroleum division maintains that roughly quarter contribution, which it has consistently done over time. Base metals, as you can no doubt see has been a smaller contributor, but this is not completely due to the lower performance this year, but also in large part due to the outperformance of the iron ore division. The other two major contributors are their coal assets. But this looks like better diversification than their peers, we like the energy aspect.

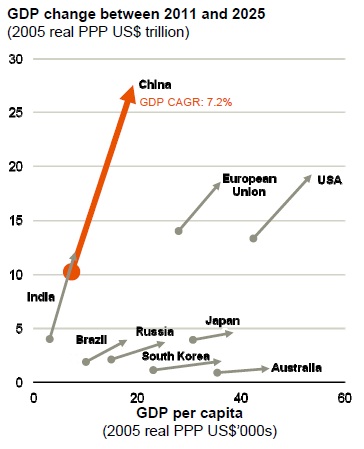

In conclusion as to whether or not you should own the company, I am first going to present BHP Billiton's outlook on Chinese growth.

So whilst Chinese GDP is forecast to be 27 odd trillion Dollars in 13 years time, on a per capita basis, whilst catching their Brazilian and Russian peers, they will still fall short. Infrastructural development is set to continue in China. BHP Billiton in their forecasting provide an eye popping number: "Chinese GDP is forecast to almost triple by CY25 with growth equivalent to 25% of current global GDP". Chinese, broader Asian and much of the developing world urbanisation will continue to buoy commodity prices over the coming half a decade at least. And in a world of choices I want to be invested in the premier mining business on the planet. We continue to add to the position through what we think is cyclical weakness. Buy.

Byron's beats covers retail, who would have thought?

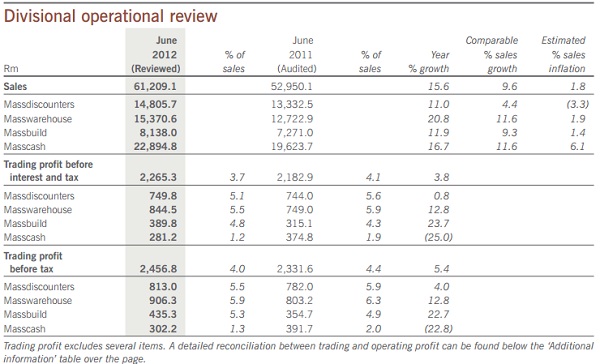

- This morning we got full year results from our core recommended retailer, Massmart. To put things into perspective let's just take a quick look at what the share price has done since the Wal-Mart acquisition which took place in June last year at R148. It has had a bumpy ride, but mostly positive all the way up to R180 at the beginning of this year. Since then it has plateaued somewhat trading around R170, where it is today. Clearly investors are waiting patiently for that big Wal-Mart induced growth spurt that the share price is so highly valued for. Let's see if these numbers can give us some direction.

For the 52 week year sales increased 15.6% to R61bn, profits increased 21% and headline earnings increased 38%. That is because last year included the costs of the acquisition. Without those costs headline earnings are only up 8.9%. These headline earnings a share equated to R6.33 affording the company a valuation of 27 times earnings, not too dissimilar to Shoprite, who reported yesterday.

This is however an example of a company who is investing heavily in the future at the expense of current profits. They have financed a record R1.7bn in capital spending on maintenance, growing operations and acquisitions. This is up 20% from last year more directly due to 3 new Makro stores, investment in the Cambridge supply chain and IT upgrades across all divisions. For a company with operating profits of R2.1bn this is big spending. Let's look at the divisional make up of the business and see where the money is made.

In case you weren't aware, Massdiscounters includes Game and DionWired, Masswarehouse is Makro and Fruitspot, Massbuild is the DIY and home improvement brands such as Builderswarehouse and Builders Express and Masscash is the retail cash and carry brands such as Cambridge and Rhino.

It is a great mix, covering all the retail divisions you would expect to grow with an up and coming middleclass and an undersupplied African continent. 8 Game stores, 5 DionWireds, 3 Makros, expanded DC's, acquisition of Fruitspot, 1 Builderswarehouse, 2 Builders Express, 5 new retail cash and carry stores and the acquisition of Rhino which consists of 15 stores were all added this year. This will certainly be earnings enhancing for a company that now compromises 348 stores across 12 countries in sub-Saharan Africa.

Even though the company looks expensive we are not deterred for two reasons. Sacrificing current profits for the future is not a reason to sell, in fact in many cases it is a good thing assuming the demand for your product can match your increase in supply. With the African consumer still off such a low base yet growing we are confident Massmart can infiltrate the right areas. The second reason, and it's one we have discussed before, is the foreign investor premium. Massmart probably have the highest of all the SA retailers because of the Wal-Mart factor. If Wal-Mart back and trust these guys then so will investors. We don't see this premium going away anytime soon so the share price should grow with earnings. We continue to add at these levels.

Currencies and commodities corner. Dr. Copper is last at 343 US cents per pound. The platinum price is higher at 1513 Dollars per fine ounce, the gold price is slightly higher at 1641 Dollars per fine ounce. The oil price is slightly lower at 96.59 Dollars per barrel. The Rand is weaker at 8.28 to the US Dollar. Risk off, in part there is catch up from weaker overnight markets in New York, those markets slipped away all day. Today we wait for the FOMC minutes of their meeting. Nice. But, as people say, the Jackson Hole Bernanke speech could be key in the very short term. Sigh. I am still going to continue to beat on this drum. Benjamin Graham said that in the short term the market acts like a voting machine and in the long term as a weighing machine. Investing is weighing, trading is voting. We are weighing folks around here.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment