Jozi, Jozi 26o 12' 16" S, 28o 2' 44" E Resources led us higher here, industrials slipped a touch, but the markets ended in the green again. Since the beginning of February again we are stuck in a zone of sorts globally. New levels that folks are getting comfortable with, people speaking of the great rotation out of fixed income and into equities. Some argue that the rally is still fuelled by easy money with a low interest rate environment. That might well be the case, but certainly risks are subsiding, still there, but further away. And let us face it, companies and countries have made hard and very difficult decisions. Some real economic news did sway the Rand bears to back off for a touch, retail sales for the month of December more than exceeded expectations. Perhaps a bounce back in the retail trade for obvious reasons, Christmas, but also as a result of industrial action ending and employees having more spending power.

Discovery had a trading update yesterday, let us do the Jackie Selebi, I mean a copy and paste job. I should stop that. After being sentenced to 15 years in jail, he was released on medical parole. I have no idea of his medical condition even if the whole process seems like a farce. So, here goes the meaty part of the Discovery trading update: "Shareholders are advised that headline earnings per share will be between 15% and 25% higher than that of the corresponding reporting period of the previous year ("corresponding period"), while earnings per share will be between 10% and 20% higher than the corresponding period."

Over here at Vestact we see healthcare as a theme that one can comfortably invest in over the coming years. As folks in the middle class start to fall into the bracket where they can both afford and view private healthcare as a necessity and not a luxury. In many ways the private healthcare industry in South Africa can be seen as a failing of the state in some regard. I can think of a few other examples, Naspers winning because the SABC has failed to provide proper content to their viewers. MTN and Vodacom over Telkom. And so on. BUT, of course we know we live in a country where the disparities between the haves and have nots are huge. So, not everyone can afford luxuries such as private healthcare, but it becomes a necessity when you get the chance of formal employment. Check what I mean, hacked from the annual report:

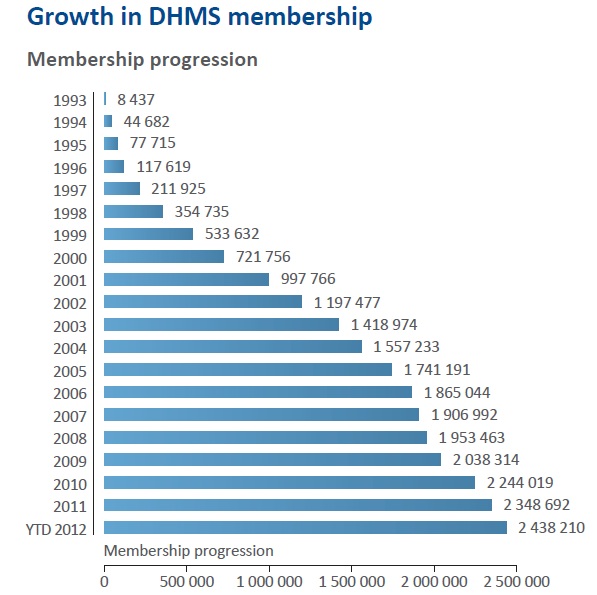

Discovery has over 2.6 million lives covered by their health management scheme. Around 312 thousand people contribute monthly payments as individuals, that is interesting, those must be self employed professionals. I would think. They are pretty revolutionary in terms of their approach to technology, the HealthID iPad app is taking off. Only 5 percent of doctors use it, according to the annual report. The company is innovative. Very innovative. Unfortunately consent has only been given by 44 thousand odd folks so far, I am one of four in my family to let our family doctor have access to all our purchases and other visits, and so on! The risks are the National Health Insurance plan and the implementation thereof and what it means for Discovery. It is a risk, but I have no doubt that the smarts there are hard at work.

It is an innovative company. They have managed to embark and gain market share in places nobody ever thought that they could. The business is run by an incredibly brilliant South African mind in the form of Adrian Gore. Those who know him say that he is humble and brilliant at the same time. The company has learnt lessons from failures before, the obvious one is the USA, but fear not, they went back, stronger than before. I like the fact that they are tackling big territories and staying away from what are heavily subsidized by the state territories. More when the results come, but we are adding this one at the fringes for clients who want more healthcare exposure. Results are due a week today.

Woolworths released their results for the 26 weeks to end 23 December 2012 this morning. There are a few moving parts in there. But some of the headline numbers look quite strong. And if you take out a few moving parts the numbers themselves look even better: "Adjusting for these items, adjusted EPS and adjusted HEPS were 35.4% and 35.9% higher respectively than the corresponding period."

And what was pleasing to see were the improving margins and cost controls both here and in Australia. OK, here are the quick numbers, comparable store sales increased 9.4 percent, including the new purchase of Witchery sales increased by 18 percent. Profits before tax rose 20.8 percent, I am thinking in this tough environment that must be pretty pleasing. Headline earnings per share increased to 164.2 cents, a 59 cents a share dividend had been declared, an increase of 14.7 percent is comfortably ahead of inflation, perhaps to compensate however for dividends tax. The after dividends tax that translates to 50.15 cents per share.

Operating margins in food were 6.1 percent, in clothing & general merchandise (GM) it was 18.9 percent, both divisions showing solid improvement. The clothing and general merchandise division contributes around two thirds of all Woolworths profits before tax, 66.2 percent to be exact. Of the group profits before tax, the clothing & GM division contributes 52.3 percent. So, it is their most important division, and in third place is their newly acquired plus existing Australian businesses. Food is 26.6 percent of pre tax profits, whilst Country Road is only 16.4 percent. Not insignificant. A weaker Rand of course helped, the Aussie Dollar has been very strong.

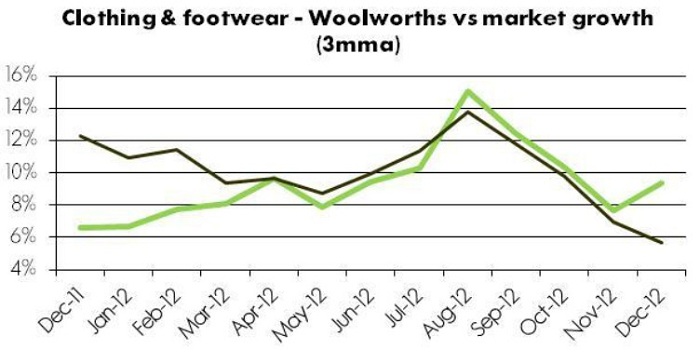

These two graphs are however the ones that stand out, these are from the investor presentation, Interim Results 2013. First, is how Woolies have been able to take market share away from their competitors in their clothing division:

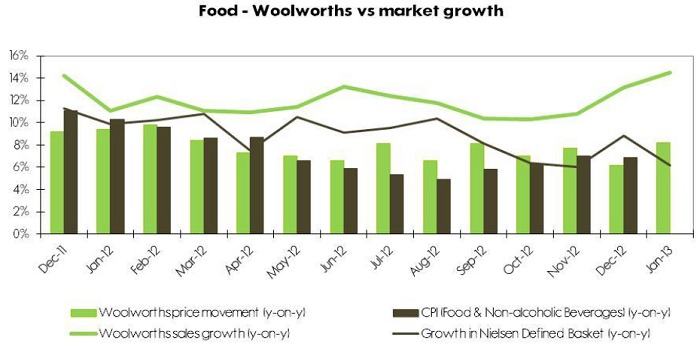

And then in their food division:

You can lie to your customers about a cheap price, or a sale, but you cannot pull the wool over their eyes if you are talking about quality. That is why in these tough times Woolies is growing their market share. That is the one reason. The other and major reason is presented in the outlook section: "We believe that economic conditions in South Africa will remain constrained, especially in the lower and middle income segments of the market where consumer debt levels remain under pressure. However, the upper income segment in which we operate continues to show some resilience. Trading for the first six weeks of the second half of the financial year has been positive, and we expect sales growth to be broadly in line with the first half." The target market of Woolies is OK. In a South African context skills are few and far between, those people with skills are well remunerated. Woolies is an excellence brand, plus they are also very innovative. They have done innovative things like reduce their relative energy bill by 27 percent from the 2004 benchmark. They have also engaged the supply chain and as far as I know are the only organic "farming for the future" chain store.

But, innovation and green technology aside, the stock does not exactly look cheap. However, to many an offshore investor, seeing that Woolies are expending to the rest of the continent, there is a big attraction. With earnings consensus looking at a middle teens growth through the next three years, you have to pay up for quality. The yield is very good, three and a half percent forward at current levels. Of course before tax. But the company has a fairly aggressive dividend policy. We like it a lot and continue to add it.

- Byron beats the streets. Yesterday City Lodge released their interim report for the six months ended 31 December 2012. I did this fairly detailed report titled City Lodge revised trading update, still good a few weeks ago when the trading update was released. It focused mainly on the property underpin and how the value increase has perked up the market cap and of course the yield has increased earnings. It also covers the fundamental analysis of the numbers.

This report gives us some more detail on the numbers as well as the actual hotel business.

"Group occupancies for the six months to 31 December 2012 increased to 63% from 60% in the previous interim reporting period. Revenue for the period increased by 11% to R492,1 million, mainly as a result of improved occupancies and the resultant increase in the number of rooms sold. Achieved room rates increased in line with inflation."

This resulted in normalised headline earnings per share to increase 30% (there was a BEE transaction last year which lowered the base) which was at the top of the range considering the update. This equated to 290.4c a share, 60% (176c) of that being paid out as a dividend.

One of the best ways to get some extra info from a results release is to watch the interview with the CEO. Here is Clifford Ross on CNBC yesterday. He makes some interesting observations on cost cuts, especially with regards to electricity. See they are replacing 40 000 light bulbs to the energy saving type. I wonder if that contract is done with Ellies? They also make sure they heat their water and do the washing at low peak times. You see there are many innovative areas they can work on and all the better for the country.

That said part of their revenue increase was due to the occupancy increase while the other part was due to inflation related price increases. 63% is still far from their all time high of 83% and also below the world average 65%. This is probably because of the massive hotel boom before the 2010 world cup. Otherwise I would expect the top low cost hotel in a developing market like South Africa would comfortably beat the global average. And I would expect the City Lodge number to certainly increase as the South African market normalises.

It was encouraging to see that their Joint Venture in Kenya has beaten their expectations, bringing in profit after tax of R7.1million and the 104 room hotel in Gabarone has been built, just awaiting regulatory approvals to start business. In the Outlook segment they say that the trend for 2013 has continued with occupancies growing nicely. They have also benefited from the African cup of Nations.

I saw no mention of management's replacement value of their property. They usually mention that in their full year numbers. All in all a good set of numbers, we are happy to be adding at these levels. South Africa is the gateway to Africa and City Lodge are going to provide the beds for those visitors.

The Mother City We are all gearing up for the president's speech here today, a little later tonight, let me hope for some love. Unfortunately progress is always constrained by limited resources. Governments have to think a little harder on how to collect more revenue, one is through boosting business activity and collecting more through growing company and individual revenue. Higher taxation through economic growth. Unfortunately the government is stuck in what a client told me a couple of days ago is industrial age thinking. We want desperately to "make things" rather than supply services. Making things would be ensuring that we have to go the low wage economy route with more factory jobs, or more mechanisation, both of which only business is fond of, the unions almost certainly are not.

If you had to ask me what the one thing that was going to change our country dramatically I would have to say that there is only one thing. Education. Skills. But that takes guts and determination and of course a whole lot of hard work. And that is not easy, it actually means knuckling down and getting the job done. But through hard work will come success. We need to be committed to up-skilling and learning more. Only that way will the workforce have more to offer.

I saw a couple of tweets on what people would like to see, this one from economist George Glynos: "Top of my wishlist for SONA: 1- More accountability for govt officials. 2 - A return to meritocracy. 3 - Start of dialogue with Business" BBC journalist and ex CNBC anchor Lerato Mbele tweeted this morning: "Zuma says priorities are Education, Health, Jobs & Land Reform. Whilst Ramaphosa on a roadshow to promote National Development Plan" You can follow on Twitter during the course of the day if you click on the #SONA2013 search tag. You will see many social issues being discussed too. The biggest issue around violence and rape, all too common a tragedy here in this country. Changing perceptions, that takes a lot of doing, but all falls back to education, the only true leveller in life.

Crow's nest. Today is an important day for European GDP, with expectations for the fourth quarter to have contracted by 0.4 percent, following the prior quarters 0.1 percent contraction. It is certainly tough in Europe, the numbers were worse than anticipated. Youngsters are unemployed, perhaps this will spur a whole new generation of entrepreneurs. The problem is that many are too reliant on the state, I am not saying that is a bad thing, but desperation has a strange old way of creating more opportunities. These are rich people problems, the problems of Africa are poor people problems and perhaps that is what Christine Lagarde was trying to say when she compared the problems in Greece to the problems of starving children in Sub Saharan Africa. I got what she was saying, the suffering lot in Greece were outraged, I understand their pain too. The other news that is unbearable to think about right now is that Oscar news.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment