To market, to market to buy a fat pig. Locally we got completely dismantled, resource stocks were taken apart. Resources sank as a collective down 3.4 percent, sending the broader market down nearly 1.9 percent. Why? Well, in recent days you have seen us talk about two things, firstly the fact that gold is losing its shine does most certainly impact on the broader commodities market. Secondly, the Fed is indicating that "things" are getting better and perhaps quantitative easing is going to end sooner rather than later. That is good for the US Dollar, that is normally not so good for commodities. The third reason could also be the Chinese authorities continued pressure on real estate. But I suspect the middle reason is the one to "blame".

Weirdly the gasoline price has ticked up every day in the US for a period longer than a month, prompting concerns from politicians. Ha-ha. Perhaps those same said folks should start riding bicycles to work, their security detail can run next to them. We should definitely start that here too, there is a huge open space in front of the parliamentary buildings, even next to the helipad. Park your bicycles there, healthy body, health mind. Which reminds me, I should start running again. There is perhaps a fourth reason too for the sell-off in commodities and specifically gold, the G20 and G7 suggesting that "currency wars" were off the table. I am guessing that the ideas that excessive monetary stimulus would wane in the coming months, that would also be very bad for the gold price. And no doubt, as I said yesterday, some shorts jumped on the already fast moving wagon.

But I suspect that it is not that easy, the Saudis are planning to ramp up oil production again, after having been lower for the last two months, in order to meet Chinese demand, which is stronger. But more importantly, as far as crude oil is concerned: US oil output increased last week to the highest level since August 1992, more than 20 years ago. The oil and gas revolution is happening in front of our eyes, jobs are at 25 year highs in the industry, it is booming. We sit here whilst the shale gas revolution is increasingly reducing the US' reliance on the outside world for energy sources, wondering whether to frack or not.

To frack, or not to frack, that is the fracking question. A question around water in the Karoo, and the farming of sheep. Honestly, if the same said folks in the Karoo were very concerned about the environment, they would all be vegetarians. And ride bicycles. But I have been to the Karoo, the Klein Karoo most. I get the sense that folks do not want their tranquil life and way of life upset by what essentially is a big business. And water is a massive issue. Sheep almost certainly do not help that equation, but who doesn't like a lamb chop? Choices. Energy independence, new industries, job creation and lastly looking for a trade surplus. Oil accounts for some 25 percent of our imports by value. But, with the current mindset around resource rent taxes and increased tampering, only the brave would take a longer term view when sinking billions of Dollars required to get the process of extraction to the levels required to turn a profit. We have the world leaders in gas-to-liquids technology. And they, Sasol, decided that the US was a better investment destination than here. Now that is a crying shame.

A Forbes article, titled How Unconventional Oil And Gas Is Supercharging The U.S. Economy,suggested that the US "unconventional" oil and gas capex by 2020 could be as much as 300 billion Dollars and could have created 3 million jobs. If the first part sounds too much like corporate greed undertones, then surely the second part should sound like music to politicians ears. If we were honestly that caring about the environment, then we would be encouraging alternative energy. Just remind me, oh yes, we are currently building two of the last internationally funded coal fired power stations. When finished, both Medupi and Kusile will be in the top ten coal power stations in the world. Ahead of us are 6 in China, one in Poland and the worlds biggest one in Taiwan. Which is set to expand by the end of 2016. The plant, the Taichung Power Plant holds the dubious record of being the world's largest emitter of carbon dioxide. Sis.

Gas power stations have much lower emissions. There could be a power station close. We could and should embark on building desalinisation plants in order to pump water from the coast, expensive, but I am sure worth it. Check this out: Desalination by the Numbers. 300 million people, or around the population of the US, relies on desalinated water. The cost however is crazy, but then again, water is life. But I see in Aussie that in Victoria (Mervyn Hughes is not the greatest Victorian, surely that belongs to Shane Warne) a desalinisation plant has just been completed at a cost of 5.7 billion Aussie Dollars. Phew. Medupi is expected to cost around 100 billion Rands, that is nearly 11 billion Aussie Dollars. Both come at an enormous cost. Where to from here locally for fracking? I suspect not too much for now. More "thinking" about it. Meanwhile a gas revolution has attracted Sasol elsewhere. Well, at least shareholders get to benefit. To understand more from the company that could help us here: Shell -> The Karoo. Make up your own mind, but I urge you to concentrate your efforts on both the practicality of energy consumption as well as energy concerns. And think about job creation and a whole new energy supply, which is great for the trade numbers and ultimately currency.

WalMart Stores, the biggest retailer in the world reported numbers yesterday morning, before the market opened. The quarter was comfortably ahead of Wall Street's expectations on the bottom line, but it missed on the top line. Let us rather than get into the Q4 numbers, and get sucked into that dreadful affliction of quarteritis, look at the full year numbers. Yes. That is good. Consolidated sales for the full year was 466.1 billion Dollars. Take a little time to reflect on that number. That is an annual turnover almost equal to the nominal GDP of Argentina, or Norway. More than South Africa. That is the size and scale of the number. Global GDP according to the IMF estimate last year was 71.277 billion Dollars, WalMart annual sales are 0.65 percent of that. Amazing. One company that employs over 2 million people worldwide. I beg your pardon, associates, not employees.

So, what is their bottom line? Well, income from continuing operations topped 17 billion Dollars, after tax margins of 3.65 percent again might not sound like a lot and a whole lot of hard work in getting there, but hey, that is what you get in retail. Whenever WalMart comes up with numbers I love using that Charlie Munger quote about Costco. "I believe Costco does more for civilization than the Rockefeller Foundation" What Charlie is trying to say is that these massive retailers do more to lower inflation and therefore make sure that the spending power of the lower income is improved by capitalistic ventures, rather than philanthropic ones. Charlie is of course Warren Buffett's right hand man, and Buffett just happened to donate a large sum of his wealth to the Bill & Melinda Gates foundations, which is a philanthropic organisation. Low prices to the masses obviously has its societal benefits.

Why would you however want to own the shares of this company? The yield is not princely, it is two and a quarter percent, whilst the earnings multiple is around 14 and a half times. So the valuation metrics look OK, but what are the growth prospects? The company paints the US consumer as still under pressure, but their own business prospects as good. "Walmart is operating in markets that offer continued opportunity for growth, both in our stores and online. With our core Walmart U.S. business operating so well, our investments in e-commerce and our international markets focused on growth and improving returns, we are truly the best positioned global retailer." In the coming years expect their incredible distribution and procurement capabilities to translate to wonderful online shopping experiences. Well, more online shopping experiences. There are also various cost saving initiatives which aims to slice 100 basis points off costs over the next five years. Now that might sounds small, but when you are talking 470 odd billion Dollars in revenue and Operating, selling, general and administrative expenses clock 88.8 billion with cost of sales at 352.5 billion Dollars, 1 percent is massive.

Their international businesses are growing revenue at between 7 and 8 percent and net income growing by about the same amount. Which is around double the growth rates in the local US business. So, I guess you could actually believe that WalMart would and could get out of this price rut, where on the last trading day of 1999 the stock traded at almost the same level as it opened yesterday. True story. All you have gotten is multiple contraction. And of course a healthy dividend flow. Walmart has increased their dividend each and every year since 1974. The market has seen earnings improve a whole lot, and have not given the stock the re-rating. But I suspect that 14 times is about all you should pay for this company. I suspect that if you are not wanting to think too hard and need a retail stock with global reach, then this company would not be out of place in a portfolio that only ever intends to hold blue chips and accumulate. The stock is about ten percent from its highs.

- Byron beats the streets. Yesterday Discovery released interim results for the six months ended 31 December. Usually we do not go to results presentations because they can be a waste of time. The whole presentation will be downloaded on the internet and most of the bigger companies are televised. Just to get a feel for management and give Adrian Gore some of my precious time I decided to go through to the presentation.

Let's look at the numbers first then I'll tell you what I learnt from the presentation.

"The period saw growth in new business annualised premium income up 12% to R5 106 million; normalised profit from operations up 21% to R1 973 million; and normalised headline earnings up 20% to R1 349 million. The period was noteworthy for its greater diversification of new business and earnings, underpinned by the outstanding performance in the UK. The UK businesses contributed R283 million or 14% of the normalised profit from operations, and their strong new business growth contributed to the embedded value growing by 18% to R33.4 billion. The embedded value growth was further driven by the positive experience variances across all the businesses. With Discovery Life cash flow positive, the group was able to achieve this growth with little recourse to capital."

On a per share basis this equated to R2.21. Earnings for the full year are expected to come in at R4.71. Trading at R67.81 after rallying 4% yesterday the share trades on 14 times this year's earnings. Certainly not expensive for a company growing this fast. But insurance companies are valued differently. They look at a metric called embedded value which is similar to NAV but a lot more complicated, determined by Discovery's actuaries. That number came at R59.26 per share. Usually an insurance company trades at a similar number to embedded value but I think because of discoveries exceptional growth prospects we are seeing a premium.

I was very impressed by the presentation. The word innovate was used more than any other and when Adrian Gore demonstrated a few new products there were gasps coming from the crowd. All of these examples were geared towards making the discovery experience easier and better for the client and that is exactly why they will steal market share from their competitors.

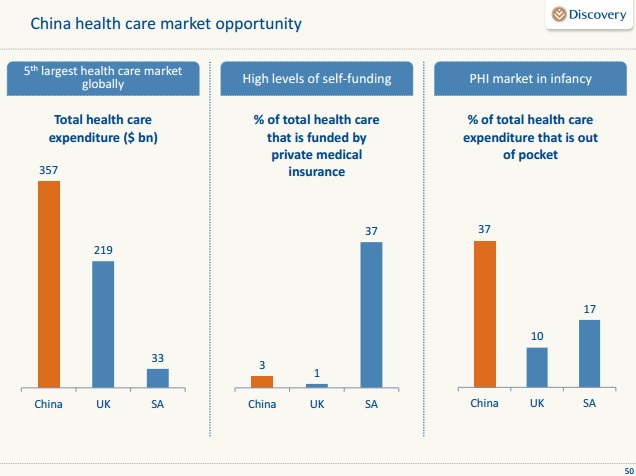

The one slide that stood out the most for me was the one explaining the Chinese market, see below. 37% of health care expenditure comes out of pocket. That is huge potential for growth. Discovery are increasing their stake in Ping An health from 20% to 25% and are very keen to benefit from the potential the Chinese market has to offer.

They are also taking Vitality to the US and have established a partnership with Wal-Mart. Vitality members will get a 5% discount on healthy foods. That theme of a good healthy lifestyle can only grow from here and will never go out of fashion. The UK business has also seen huge growth as the NHI suffers from austerity and private healthcare becomes more prominent.

With very exciting prospects internationally, an amazing innovative and creative model which is stealing market share, an extremely astute management and operating in a sector that has a very bright future we are happy to be adding at these levels.

Crow's nest. Markets are flat at midday. Retailers are lower, resources seem to have caught a bid. Some more German sentiment numbers have beaten expectations. Italian elections this weekend people, I suspect that the Italians are going to show us again the push back on austerity.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment