Jozi, Jozi. 26o 12' 16" S, 28o 2' 44" E. Wow, I did not really expect such an astonishing rally at the end, although there was great Grelief, there was anxiety about Spanish bond yields again spiking to Euro era highs. Spanxiety? Urban dictionary suggests that the word is way too rude, I had no intention of being rude, so perhaps we should call it what it is, Spailout. And who knows, Italy might be looking for cheaper credit sooner rather than later. All of this going on in the midst of the most important football tournament in Europe, which is exciting, and at the end of the week possibly the most anticipated match in an absolute age. The irony of it all, Germany against Greece on Friday evening. As we speak (write?) the new not yet formed government of Greece are asking Germany for more time for implementing the austerity measures. Which must leave the Queen of Europe shaking her head, in a match that we must term, the mother of all sovereign debt struggles.

Back to markets here locally, the Jozi all share index added a whopping 478 points, or 1.41 percent to close up shop at 34438 points, with gains across the board for all of the major indices, the banks roared over two percent, the retailers a more muted 0.29 percent better, the all important resource stocks added over a percent and a half, whilst the only noticeable losers were the construction stocks, down just shy of a third of a percent and the gold miners which sank just shy of a tenth of a percent. General industrials added nearly 1.2 percent on a generally good day for all and sundry. We closed on the ALSI a mere 43 points away from the early May all time highs. Tough going? Seems like it, but hey, the numbers tell a different story.

Naspers released a trading statement yesterday, it is complicated, because there are three different measures. That is often not a good sign, but be that as it may, the company considers what they term "core headline earnings" to be the true measure. And by that measure, on a per share basis, the company expects to increase core earnings per share by between 10 to 20 percent from the last years 1612 cents. So, in the middle of that range, 1853 cents per share. So, at the current share price of 46760, the price looks completely stretched. But. But. Not so fast, the valuation is in part earnings, and in part an NAV type valuation. We have covered this before in results, check it out: Naspers valuations, that was from last year, almost a year ago, that coincided with the results there. Results are in 8 days time, that would be the true test again of what the company should actually trade at, or be worth. Because often, and I hear this, folks suggest that the Multichoice business and the just less than 35 percent stake in TenCent make up the rest of the entire market cap. So, basically, you get the rest. But that is a simple and easy way of valuing what is a complex business.

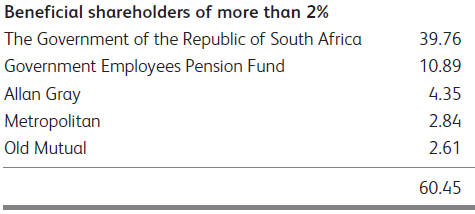

Telkom, still trying to touch tomorrow, but at yesterdays share price. The BusinessDay has a story that suggests that the state are going to discuss this one in their policy pow-wow as to whether or not the asset is strategic. And whether or not it should be re-nationalised. Phew, that is why the share price is up a lot today, around four percent better. But what would they have to pay? Well, there are 520,783,898 shares in issue and government own a 39.76 percent stake which translates to 207,063,678 shares. So, if that were the case, government would have to buy the other 313,720,220 shares that they do not own in order to take the whole thing off the market. Let us suggest for a second that government pays 23 Rand a share, and I am not too sure that minorities would accept that, then the price tag for the rest would be 7.21 billion Rand. That would come from where? Total GDP at market prices in 2011 for South Africa was 1.895668 trillion Rands. So, this is not big, but our total budget is one trillion Rand, why would you blow around .75 percent of the total budget on buying this? And the way that we see it here in the office, the mobile entrants, of which two are dominant here in South Africa, are rolling out their infrastructure faster and with less red tape. Fewer meetings about how to do it, just plain old doing it. Execution and not talk, we are pretty good at that in South Africa.

Byron's beats is again focussed on the construction sector. I must be sure to buy him some Lego for Christmas.

- Cees Bruggemans Chief Economist at FNB comes up with some very interesting material. Here he covers some data called the FNB/BER construction confidence index which of course looks at the health of the construction sector in South Africa. Here it is. Now this is a sector that is very important for the economy and especially our jobs market. We are also invested in the future of this sector via PPC and Cashbuild.

So what does the report tell us? This is the 3rd consecutive quarter where the index has risen and is the highest it has been since the end of 2009. "The 2Q2012 results suggest that the recovery is gaining momentum with construction activity in particular picking up noticeably. Despite this, there is still reason to believe that this recovery remains fragile."

That is good news. We saw signs of this near the end of last year where we saw a turn in cement sales. The construction index is up over 12.5% for the year so far which means the market believes in this recovery to. It is off a low base however. Just as a reminder the sector was down 43% in 2008, up 8.2% in 2009, flat in 2010 and down 25.6% last year. Let's carry on with this report.

"Capital expenditure (capex) from provincial governments remains robust. During the 2011/12 financial year (ended on 31 March 2012) provincial capex was 21.7% higher year-on year. This momentum likely continued with a number of projects focused on the healthcare sector and water and water waste management being initiated.

In contrast, municipalities continue to struggle. Only 41% of the total municipal capex budget had been spent during the first 9 months of the financial year (until March 2012). However, some work could have flowed from municipalities as they push to spend more in the last quarter.

Public corporations saw an increase in civil construction activity with new projects from the TCTA and ACSA in particular coming on line.

However, construction activity from the private sector likely contributed less with mining production slowing and some mining firms holding back on expansion plans."

Unfortunately the sector is still very dependent on the public sector. With rumours of bankruptcy amongst municipalities and story's like the Sanyati one who are insolvent because they have not been paid by government, you can see why they say this recovery is fragile. We have to see a pick up in the private sector. PPC did mention in their results presentation that private housing, which is responsible for 50% of cement sales, was starting to pick. With interest rates at historic lows and a growing middle class I tend to agree. There are still many headwinds for this very cyclical sector but having read this report I remain confident that we have seen the bottom of the cycle.

New York, New York. 40o 43' 0" N, 74o 0' 0" W. After opening much lower, stocks proceeded to pare losses and then mostly hang onto some slim gains. The S&P 500 managed to just eke out a gain, up nearly 2 points or 0.14 percent on the day to close at 1344 points. The nerds of NASDAQ had an even bigger gain, adding nearly four fifths of a percent, driven by a strong move from Apple, the stock was up over nearly two percent. The Dow Jones Industrial average bucked the trend, losing 25 points on the day to 12741, banks and energy lagging there. Plus also some technology giants, HP sank nearly three percent, the stock is now down all of 18.3 percent year to date and is the worst performing stock in the Dow this year. The best performing stock is the unlikely Bank of America, up an astonishing 39.5 percent YTD. But, over 10 years, Bank of America is down an astonishing 78 percent. Most of that was over the last five years. HP on the other hand is up only 12.6 percent over the last ten years. IBM over the same time frame is up 153 percent, crushing the dogs of the Dow.

Strangely, the Dogs of the Dow is an investment strategy that suggests that at the end of the year, you must take the top ten best yielding stocks in the Dow Jones, and buy those. The idea is that blue chip companies included in the index will pay higher dividends over time and you therefore are getting a bargain, over the longer term. Check it out, somebody actually maintains a daily table and spreadsheet to help folks make these very easy decisions: Dividend Yield for Stocks in the Dow Jones Industrial Average. All 30 stocks in the index pay a dividend, which was not always the case. IBM I am guessing are going to have to think about a stock split soon, their price is nearly double that of the next most important stock, because the Dow Jones is a price weighted index.

Do we even want to talk about the Microsoft Surface tablet? I guess we should and we must, the "Surface" was unveiled by CEO Steve Ballmer. The device weighs slightly more than the current iPad (the new iPad) but has a bigger screen, 10.6 inches compared to the iPad 9.7 inch screen. The pricing will be similar to that of other options out there, and by that I suspect that Ballmer means the Samsung Galaxy and the Apple iPad. What is quite cool is that there is a magnetic cover that doubles up as a fold down keyboard. And it can connect with printers, and it has a USB port. But, the expensive part will be that it runs a version of Microsoft 8 and office, so that licence part will have to be paid for by the user, which could mean that it might be more expensive that an iPad. As the WSJ points out though, if this is meant to replace the PC at home, then how do the manufacturers of PC's feel about this hardware muscling by Microsoft? Not too sure how they feel, but my thinking is that they do not feel altogether excited by this, HP, Dell and the like. I guess the good news for Intel is that their chips will be used in these products.

Microsoft is still a beast, with a market cap of 250 billion Dollars, over five years the stock is flat, but has paid a regular dividend, the current quarterly dividend is 20 cents per share, up from 10 cents five years ago. You would have got 182 cents if you had owned them over the same period. I swear to you that I ran a simple one year valuation model assuming that a growth rate of 8 percent was acceptable and got to about the current share price, in fact just below at 28.37 Dollars. The stock currently is at 30 Dollars in the pre market, indicating that whilst there might be haters for the device, Mr. Market thinks this is about neutral. Check out the presentation, which was live blogged by the fellows over at the Business Insider: Microsoft Announces Its Own Tablet, The Surface. Am I sold? No. But the stock still looks cheap man.

Currencies and commodities corner. Dr. Copper last traded at 340 US cents per pound. The gold price is last at 1631 Dollars per fine ounce, the platinum price has crept up to 1485 Dollars per fine ounce. The oil price is last at 83.03 Dollars per barrel. The Rand is last at 8.25 to the US Dollar, 12.93 to the Pound Sterling and 10.46 to the Euro. Stocks in general are being sold off today, after having touched an all time high earlier in the session.

Parting shot. Check it out, as Randy Jackson would say, he might add dog to that, but it is an endearing dog. The Jozi all share index touched an all time high, 34561.99. It would have been better if it was at 34567. But there you go, in the face of what is still poor news, we continue to see the indices head higher. Because Europe will solve their problems, they are not insurmountable, they are dire at present, but so were many moments in history. In five years time we will look back at the European sovereign debt crisis in the same way that we look at the subprime mortgage mess in the US, that period there. And Europe will be a more united place, not less so. Question: Is Greece still in the Euro zone? Answer: Yes.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440