To market, to market to buy a fat pig. I read yesterday that you are not supposed to trust Chinese data from the official sources, I guess because there were some invoicing scandals at some point. And that goes to the very core of our industry, trust is everything, it takes years and years to build and can be eroded in seconds. Think of somebody like Jon Corzine, who was the CEO of Goldman Sachs from 1994 to 1999, and the governor of New Jersey for four years. But he was then the CEO of MF Global, where the company used clients money to cover the firms liquidity shortfall.

Phew. That is disgraceful, really. All of that goodwill and energy built into gaining trust of the investment community and broader society evaporated. And whilst it became apparent that by August 2012 that there would be no criminal charges brought against the management, it is tainted, their reputations. So if the numbers from the Chinese authorities are incorrect, does any authority take any heat? Or are the Chinese, hey, we made a mistake once, at least we uncovered the mistake.

Woolworths, one of our preferred retailers, reported numbers for the 26 weeks to end 29 December 2013. This is the first half of their financial year. Byron said that I stole his thunder because he wanted to write up about these numbers, so I had better make sure that I do a fine job, or else...

Firstly, and as strange as it sounds, what does Woolworths actually do? The simple answer is that the company sells clothing, food and general merchandise and it is fair to say that they are a premium brand in South Africa, in a sense soft luxury in the food department and they posses upmarket internal brands that certainly have been winning market share. Woolworths strive for quality over quantity, as a consumer I have never had a problem with any of their products, but just the other day I fielded a call from a Cape Town based client who said that the Woolies quality down the road from her (food) was poor. Michael tells me that often the Woolies in his home town has bare shelves on a Saturday by lunch and the poor staff have to shrug their shoulders. In Gauteng and in particular around where I work and live, I never have that problem and I am very spoilt with high quality (dare I say world class) products from Woolies.

The only point that I am making is that you must be careful to translate your own experience (good or bad) into whether or not the company is a good investment. Although that of course does define whether or not you, as a consumer, are going to use their services or buy their products? Of course it does and Woolworths have always prided themselves on being able to deliver the best quality product at the most reasonable price.

Numbers time, because at the end of the day the company could sell manure and be profitable, what matters to their shareholders is whether or not they manage to maximise profits. Sales for the half registered 19.4 billion Rand, a 16 percent change on the comparable period. Profits for the period registered 1.567 billion Rand, an increase of 22.1 percent. The company paid nearly 600 million Rand in taxes, thanks Woolies for contributing to the national fiscus, or rather thanks to the customers, who directly make sure that the company exists. The famous exchange between Henry Ford (the second) and union leader Walter Reuther, in which Ford pointed to automated machinery on the factory floor and asked Reuther how he was going to get the robots to pay union dues. Reuther snapped back with a fabulous answer, in the form of a question, Henry, how are you going to get them to buy your cars? Quite.

Headline earnings per share increased by 17.2 percent to 192.4 cents, the dividend declared for the half was 101 cents, generous payer Woolies. After tax that amounts to a little more than 85 cents (85.85), payable on the 10th of March.

On a segmented basis, Woolworths foods turned over 15.3 percent more than the prior period, just shy of 9.5 billion Rand, with profits before tax adjusted increasing 16 percent to 586 million Rand. So let me get this right, the company paid more in taxes than they earned in their foods business? But the food division as you know is not very profitable, so whilst the clothing and general merchandise division grew profits by 7.4 percent, Country Road with a 51.9 percent increase in profits are breathing down the Food divisions neck in terms of absolute profits. But yet is only 41 percent of sales. So that just goes to show you how much more profitable clothing is.

We did however speak about the inclusion of the Witchery business inside of this reporting period, Country Road, which reports as the Australian business. In Australia this is a premium business, as you well know, the clothes at Trenery and Country Road are not cheap. There are of course huge currency implications here, the Rand has weakened significantly over the last year to all the major currencies. Not that the Australian Dollar has had a good time of it lately, this morning there was an Australian unemployment read that was weak, their worst level in ten years, which topped six percent. The horror of it all, but I guess that these are rich people problems. Over the last year the Aussie has gained 8.4 percent to the Rand. Over the last five years, it is much more dire for the Rand, the Aussie is 53 percent stronger. Phew.

In the commentary: "In Australia, where consumer confidence remains cautious, there are signs of an improved retail market and we expect sales to be ahead of the market." so whilst we have to pay careful attention to the consumer here in South Africa, with Woolworths business in Australia we will have to do the same. In South Africa, the commentary is that the lower and middle income groups are under pressure and consumer associated debt in those LSM classes remain elevated. But about their core customer base: "the upper income segment in which we operate continues to show resilience. Trading for the first six weeks of the second half of the financial year has been positive, and we expect sales growth to be broadly in line with the first half."

So what now as an investor in Woolworths? I guess the cycles are unavoidable as consumers, they come and go as interest rates rise and fall. Consumers repair their personal balance sheets when their financial situations look dire. The reaction to what look like decent results is that the stock is down over three percent, and trading at the same multiple as the rest of the sector (forward), I think that it offers good value at these levels. It is a growth company operating in a tricky environment, but they have the right mix and great management. Strangely Ian Moir is listed as Australian, he has a deep Scottish accent, perhaps some United fans would want David Moyes to naturalise as an Australian. Give the man a break, a couple of years at least! Ian Moir on the other hand has another tough challenge on his hands, but I think that he is definitely up for the challenge.

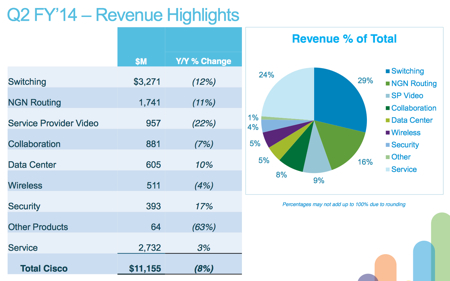

Byron beats the streets: Cisco quarterly numbers

Last night we received quarterly results from Cisco which again looked fairly muted but above analyst expectations. Revenues were down 7.8% to $11.8bn. Net income for the period was down 54.5% but that was because there were a few once off charges. From continuing operations Non-GAAP net income came in at $2.5bn which was down 7.4% from this quarter last year. This equated to 47c per share. The image below pretty much summarises where and how this business makes money.

Yet again the market was disappointed and the share price declined 4% after the market closed. John Chambers just seems to drone on and on about the same thing.

"We delivered the results we expected this quarter. I'm pleased with the progress we've made managing through the technology transitions of cloud, mobile, security and video. Our financials are strong and our strategy is solid. The major market transitions are networking centric and as the Internet of Everything becomes more important to business, cities and countries, Cisco is uniquely positioned to help our customers solve their biggest business problems."

Wow, the man is bullet proof and said something very similar during the last presentation. We are patient investors but this has been his tone for the last 3 years. I still really like the thesis behind this stock as an investment. They provide the routers and the servers that connect big businesses to the internet. They also service this hardware. It is a great margin business but it is becoming very competitive and these margins are getting squeezed. Especially in developing markets.

The company needs new management and fresh ideas in my opinion and the fact that Chambers is both chairman and CEO does not sit well with me.

Having said all this, the stock is cheap. Earnings expectations are for $1.86. Trading at 21.90 we are sitting on forward earnings of 11.8 times. Plus they are sitting on $47bn of cash which is nearly 40% of their market cap. The fundamentals are strong and I'd expect demand for their product will grow, especially as people expect faster and more efficient internet services. I would hold this one but I wouldn't be adding until we see some shifts in management.

Michael's musings: Growth is around

The Bank of England has revised their forecast for the growth in the UK economy from 2.8% to 3.4%. That is a pretty sizeable jump and is very good news considering that the EU as a whole is expected to only grow by 1.1% in 2014.

Adding to the great news for investors and general population is their forecast of reaching the 7% unemployment mark at the start of this year, two years ahead of last year's forecasts. Good growth and lowering unemployment also reduces the risk of European economies slipping into deflation.

The Germans also increased their growth forecasts for 2014, this time not as impressive but you will always take an increased revision over a lower revision. The German government increased their forecast from 1.7% to 1.8% for 2014. Their economy is expected to increase exports by 4.1% (a positive sign for global growth) and increase their imports by 5%.

Driving around Sandton there are many exciting new buildings, which is exciting for me because when building starts it is a good indication that people have confidence in the future. You don't spend billions of Rands on a new building if you are worried about the future. Below are two pictures of new building sights. The first is of an old Standard Bank building being torn down and the second is an old Holiday Inn.

Yesterday the WSJ had an article on trader's looking at using lasers to increase their trading speeds by nanoseconds. The recent history for traders looking for speed has evolved from fibre optic cable, then to another fibre optic cable which was slightly shorter than the first, then to microwave and later millimeter-wave transmissions. For traders who are paying millions in order to gain nanoseconds, the time period between monthly data releases must feel like an eternity. Highlighting the short term nature of some of the big players in the market.

Home again, home again, jiggety-jog. Lower here to begin with. The state of the nation tonight, are you going to watch? You should, you know, because whilst it may not appeal to you, you have to care.

Sasha Naryshkine, Byron Lotter and Michael Treherne Email us Follow Sasha, Byron and Michael on Twitter 011 022 5440

No comments:

Post a Comment