"I do not think that BCX offers them, Telkom, anything new at that price. I do think that it offers the institutional shareholders of BCX and the management team a chance to exit. A 20 percent premium? That is the best part of the deal for BCX and possibly (for me) the only point in amongst the seven that makes sense. Telkom proposes to fund the transaction from their side, all cash, which means that they will have to raise the money on top of their existing cash. And no doubt add to their existing debt. Am I the only person who feels this way?"

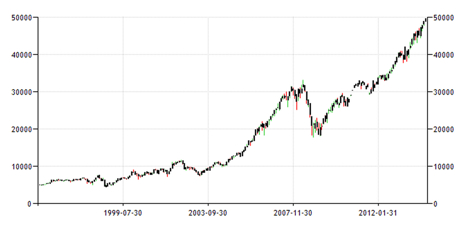

To market, to market to buy a fat pig. Well, yesterday we crossed that mark, the 50 thousand mark on the all share index. So at least we have breached it now and can stop talking about it, a level as if it is some amazing and dizzy height. Perhaps we should rebase the index back to 5000 points and then everyone can stop feeling so dizzy. Sadly I cannot find too many graphs of the long term performance of the JSE, but I did find this one from tradingeconomics.com, nearly 20 years old now, from the beginning of 1995 to present day.

As you can see, less than 20 years, and the index (without the benefit of dividends) is up ten fold. There is of course that massive blip in the middle there, see that? That felt terrible at the time. It really did. But it turns out that it would have been more terrible to sell. So where does that leave you, as the investor? I mean, check it out, Bespoke have recent data that suggests to them that on a long term S&P 500 Historical P/E Ratio the market could be cheap or expensive. What is interesting there is that 10, 25 and the long term averages (from 1929) all differ. The conclusion leaves it all up in the air: "equity valuations are not on the cheap side of the spectrum. They're also not that expensive either, though." Err...... Thanks.

But surely, and I am thinking a little out loud here, the long term averages do not reflect the impact of the Cold War? I mean, the Moscow Exchange only really started in 1992. So the long term average does not include countries which were involved with communist activities. We forget, but the Iron Curtain was still "up" one quarter of a century ago. Those pictures of "the wall" being smashed down by people from both sides are still engrained in my memory. That fellow with the peroxided big hair and weird jeans and giant hammer. Mind you, there were lots of those. But think about the longer term issues, access not only for companies to new territories, but also companies having access to capital internally. The Chinese economic miracle, currently we are seeing huge interest in African countries, there are MANY more people in the world, I keep making this point over and over.

In 1929 there were a little over 2 billion people on the planet (passed in 1927 for the first time). We crossed 4 billion in 1974. 5 billion in 1987. OK. 8 billion is expected in 2027. In large part this is as a result of improved nutrition and better medication for all, although we still live in a very unbalanced and unequal world. For example, I saw a little piece in an analysis on thermal coal that went something along these lines: The electricity demand from New York (8 million strong) is the same as the entire populations of Bangladesh and Nigeria combined. Collectively those populations are nearly 320 million. I mean, that is completely astonishing. No. Mind blowing. For each and every one persons usage of electricity in the Big Apple is equal to 40 people in Nigeria or Bangladesh's usage.

Granted that New York is quite possibly the most built up and advanced place anywhere on the planet, and I am sure that in rural America somewhere electricity usage is similar to that of an emerging market. In terms of total electricity consumption by country, the USA is second globally. China is first. Between the two, they account for around HALF of the global usage, at least according to the Wiki data supplied. South Africa actually sits in 17th place, so we are pretty intensive users. But in terms of consumption per capita, we fall into company with Libya, the Ukraine, and even China, believe it or not. On a per capita basis countries like Austria and Singapore are double what we are. Understandably countries like Norway, Iceland and Canada have the highest electricity usage on the planet.

But how does 50 thousand points on the local index and increased electricity (and indeed unbalanced electricity usage) demand globally tie up? Well, the point is simple. I can imagine that everyone wants an easier and more advanced life that has better services. Better medical care, better schooling, better municipal services. But we all need to be richer in order for that to happen. And companies nowadays are more global than ever before. But to answer that valuations concerns question, companies have possibly built in more efficiencies in the last five years globally than at any time in the last quarter of a decade. That is probably why labour has not been the winner in the recovery, mechanisation is real and happening. Unfortunately for labour, and that possibly counts for all of us and our occupations, we are wanting to price ourselves out of existence. Existence in the labour form of course. Keep calm and stay invested, even if equity markets sell off (which they always do) remember what you own. Paul said it well in a tweet yesterday:

The South African stockmarket (JSE Alsi) is almost at 50,000 points. That has a nice ring to it. We are fully invested as usual. #winning

— Paul Theron (@paul_vestact) May 20, 2014

Pff... I am not too sure what to make of the Telkom and BCX hook up and revisiting the past here in a sense. Last time the competitions authorities blocked this. Last time around both companies were in a stronger position, financially speaking. BCX's star has faded in recent years, revenue growth barely matches inflation and margins are not too dissimilar to what we are seeing in the construction sector right now. Really low, somewhere around two percent. And Telkom are wanting to pay around 20 times earnings for a business that has barely grown earnings. Telkom themselves are not expected (from the analyst community) to grow earnings at all, in fact they are expected to go backwards, earnings wise. So whilst Telkom might look cheap, at the same price they are expected to be more expensive, because the analyst community expects earnings to decrease by double digits next year and then high single digits the year after that.

I do not think that BCX offers them, Telkom, anything new at that price. I do think that it offers the institutional shareholders of BCX and the management team a chance to exit. A 20 percent premium? That is the best part of the deal for BCX and possibly (for me) the only point in amongst the seven that makes sense. Telkom proposes to fund the transaction from their side, all cash, which means that they will have to raise the money on top of their existing cash. And no doubt add to their existing debt. Am I the only person who feels this way? It feels like a desperate attempt to diversify away from a shrinking business towards one that is very competitive and low margin and cutthroat. Not skills that the Telkom machine has always possessed, being able to upend their competition. Anyhows, all shareholders have been canvassed no doubt, for the time being Telkom are facing other problems as they continue to slimline their workforce, the CWU is fighting the pending retrenchments at Telkom. Not businesses that we are invested in anywhere.

Home again, home again, jiggety-jog. US futures are marginally higher, German IFO business confidence numbers were lower than anticipated. It is a holiday in the US on Monday, I have no idea what that means for markets at all. We have crested the 50 thousand points mark again, it would be *nice* if the equities market could stay there for the weekend, we will see!

Sasha Naryshkine, Byron Lotter and Michael Treherne

Follow Sasha, Byron and Michael on Twitter

011 022 5440

No comments:

Post a Comment