"What is pretty amazing is that revenues increased by 33 percent when compared to the corresponding Q3 from the prior financial year. That is enormous. What is bigger is that earnings were 45 percent more. All from the biggest company in the world, not a start up. This is also the fastest growth reported in three years, that makes this even more astonishing."

To market to market to buy a fat pig. Over the seas and far away it was about earnings, and specifically poor ones from IBM which recorded their 13th successive quarterly revenue decline, across all geographies at that. Seeing as this is a big stock holding of the Sage of Omaha, Warren Buffett, there is a little more attention when the stock price is performing poorly against the backdrop of poor company numbers. IBM is certainly not a dinosaur, there are however concerns that they are missing too many tricks and struggling, like many of their competitors in the internet age.

An ex employee of the company puts it less politely: IBM is so screwed. I think that he may have personal issues, his points are however well made. In the same way that the Dow Jones does not have Google, it has IBM as a constituent, the stock was down nearly 6 percent by the close, dragging the blue chip index down a percent by the close. The nerds of NASDAQ closed one fifth of a percent down, over the last five days tech stocks have trumped blue chips by nearly three percent, all thanks to new tech, Google versus old tech, IBM. Expect that to stay like that even today as Apple is a constituent of both indices.

Anxiety seems to have abated about an almost certain rate hike in September now, you know our views on that, it changes very little for the outlook of stocks. In fact rates going up signals strength in the underlying economy, when we turn our eyes locally here, expectations are for a rate hike tomorrow. And I do not believe that it is warranted. Are we reacting to an inevitable rate hike in the US and worry what it may do to currency markets? Not too sure, with the recent move lower in oil prices and the Rand sort of stabilising, it seems that inflationary pressures have abated. And if all the conversations that I have with people out there about the economy, then it is certainly not demand that is going to drive inflation. It looks fairly quiet out there.

At the end of the session the All Share index (Jozi, Jozi) ended down 0.16 percent, just below 53 thousand points. Financials were the biggest losers, there was a big bounce in gold and platinum shares, still, they need to add fifty odd percent from here just to break even for the year. Sigh. How times have changed. And at the moment, wage negotiations are not going well in the gold mining sector, we are looking at signs of a strike, perhaps even a long and protracted one. Paul mentioned that unfortunately in cycles of business this is hardly favourable for anyone and normally represents how dire things really are when labour is at this point. He is right, gold mining in South Africa is about to get a whole lot harder.

Company Corner

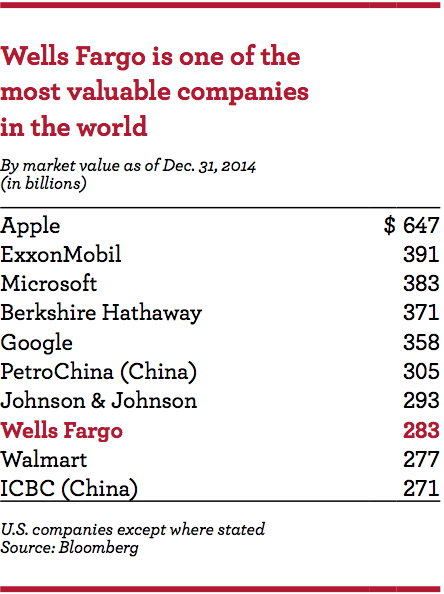

Last week we had the second quarter results from Wells Fargo, who you will probably know as one of Buffett's "Big Four stocks". Berkshire Hathaway owns nearly 10% of the company which currently has a market cap of $299 billion. Here is where it ranked in size at the end of last year:

Here are the numbers that count: EPS up 2% YoY; Revenue is up 1% to $21.3 billion for the quarter; loans up 1% to $870 billion; dividend is up 7% and they repurchased 36.3 million shares. Net interest margin dropped to 2.97% from 3.15% a year earlier. Net Interest margin is the main number to look at when it comes to banks. It is the difference between the interest that they have to pay out to their depositors and the interest that they receive on lending out money. So the bigger the Net Interest margin, the more profitable the company. Given the low interest rate environment, the Net Interest Margin has been pushed lower as their longer term interest received on loans has been substituted by lower interest rates.

What impact does a FED increase of interest rates have on Wells Fargo? My first reaction would be a slightly more negative impact, due to customers having to pay higher interest, they would demand less of the product (loans). It is defiantly a blurry cause and effect in the case of many banks but after doing much reading on the topic I think Wells Fargo will benefit for interest rate hikes. Here's why:

1) Interest rates going up means that the economy is stronger meaning that there are less bad debts but also that corporate America becomes a bigger customer.

2) Currently 26% of deposits with Wells Fargo is non-interest generating, which means that when rates go up they can take those deposits and lend them out at a higher rate and still not have to pay for them. This will have a nice boost on their Net Interest margin.

Banks are considered a good proxy for the economy in general because the better things are going in the economy the more people spend and the more people borrow. This is a company that we would buy given that the long term outlook for the US is bright and that interest rates are going to start rising soon. The added bonus is that the major shareholder is Buffett who likes a more 'boring' approach to banking and an earnings stream. The result is less 'blackbox' earnings and less exposure to fancy, complicated products that can make short term profits but have a tendency for blowing up. They are not going to shoot the lights out but should continue to grow and distribute more profits to shareholders each year.

Mediclinic rights issue

Ok, listen up shareholders, Mediclinic announced their rights issue yesterday. This is of course in relation to their purchase of a 29.9 percent stake in Spire Healthcare from Remgro, who had the immediate resources to do the deal first. Mediclinic are going to be raising 10 billion Rands. Here goes, per 100 shares that you hold, you are going to get 12.80145 rights at 90 Rand a share. Just a reminder, the share price is currently at 106 odd Rand, so it makes sense to follow your rights. So around 11 percent of the value of your shares currently, that is what you have to factor in for the rights. Remgro are underwriting the rights issue.

Here are the dates, it looks a little tight. The stock goes ex rights after the close of business on the 31st of July, which is next week Tuesday. The rights issue closes 21 August, the new shares start trading on that Monday, the 24th of August, in around four and a half weeks time. Like I said, we do not have that much time to work with here. We will be in touch with shareholders, we are recommending that all shareholders follow their rights.

Hey Apple

The biggest company in the world by market capitalisation (and cash position) reported numbers last evening after the market closed. I am talking about Apple Inc. A company that makes fine products, their most well know being the iPhone, in the current cycle the 6 (and 6 plus) has been a real amazing product very well received by customers all over the globe. At first take revenues of 49.6 billion Dollars for the third quarter are a beat (and a record), the company reported profits of 10.7 billion, also a record for the third quarter. Earnings of 1.86 Dollars a share. Gross margins improved to 39.7 percent, also better than the corresponding quarter.

What is pretty amazing is that revenues increased by 33 percent when compared to the corresponding Q3 from the prior financial year. That is enormous. What is bigger is that earnings were 45 percent more. All from the biggest company in the world, not a start up. This is also the fastest growth reported in three years, that makes this even more astonishing. iPhone sales are three times the growth rate of the rest of the smartphone market, growing in all their markets, emerging and advanced. And what is pretty astonishing, in terms of surveys done by a crowd called ChangeWave, 86 percent of iPhone owners plan to get another one. Whilst you may say why isn't it 100 percent, for other smartphones the same survey crowd found other brands have a 50 percent repurchase intent.

China drove smartphone sales, comparable quarterly unit sales up 87 percent on revenue growth of 112 percent, now at 13 billion Dollars it represents 26.2 percent of total sales. Yet other smartphones grew only 5 percent in the same time frame in China. Pretty astonishing and perhaps pent up demand for the product. Mac is also making inroads in a falling PC environment, growth of 9 percent may not sound amazing, against the backdrop of the rest of the market contracting 12 percent it is astonishing. All in all, the company sold 4.8 million Macs. In the services division, the company set another quarterly record, 5 billion Dollars in revenues. So roughly ten percent of revenues come from this division. Inside of services, the App Store had its best quarter ever, revenue growth of 24 percent. App store revenue in China more than doubled. Wow.

Cash has popped above 200 billion Dollars for the first time, with cash and cash equivalents at quarter end 15.319 billion Dollars, short-term marketable securities 19.384 billion Dollars and 168.145 billion Dollars worth of long term marketable securities. Add those up and you get to nearly 203 billion Dollars. Just of cash resources. When measured against their likely opening share price and by extension market capitalisation of 708 billion Dollars, you get around 28.6 percent. Of just cash. 89 percent of all of this is offshore.

The company could buy almost anything they want, yet their largest ever transaction has been to buy Beats by Dre (I have a pair, they are incredible, amazing), 3 billion Dollars in total. That is the biggest deal ever, which is around 0.42 percent of their market cap currently. Of course more back then, you get the point I am trying to make, which is that they rely on internal resources to make desirable products. Talking of cash resources, the 52 cent dividend is payable 13 August, the stock goes ex div on the 10th. That is quick, when you have the resources I guess anything is possible. Apple pays currently around 12 billion Dollars a year of dividends. Wow. That is more than all the market caps of the JSE bar for the top 17 shares.

The Watch? How is that going? Without giving numbers specifically, estimates that I have read suggest that the company sold 1.9 million units. Tim Cook on the conference call chatted about various medical uses already, from chart to dosage use (and reaction of patients) to monitoring of cancer patients receiving care at London King's College Hospital. Cook also spoke of being a good way for doctors to monitor hypertension patients daily, minute by minute. Beyond the obvious medical monitoring comes fitness applications. There is a renew in the coming months for the operating systems, the watch so far has received a 97 percent customer satisfaction rate. The other three percent of people have sausage fingers.

Apple music has been launched in over 100 countries, as a family I have signed us up, it works beautifully I have found. Is it the death of radio as we know it, at least music radio with everyone with an iPhone and an internet connection (the two go hand in hand) able to listen to exactly the same music at the same time. Michael had a friend who was excited about that, I'm getting the same music as they are in New York, London and so on.

Why did the stock take a pounding after hours? One of the reasons is that whilst revenues topped estimates, iPhone sales, their flagship unit, were slightly lighter than anticipated coming in at 47.5 million units. Another reason is that guidance was lighter than the market had anticipated, or had pencilled into their models. Revenue for the fourth quarter is expected to be between 49 to 51 billion Dollars (4th quarter last year was 42.1 billion), gross margins are expected to be 38.5 to 39.5 percent. That does not sound too different to the quarter just past, the growth rate is still tremendous.

So you want more? On the conference call Tim Cook answered a question that I think is relevant here, only 27 percent of people have upgraded from the last cycle, meaning that potentially 73 percent of all iPhone owners own a 5 or lower model. Not everyone gets a new phone, it gets handed down, bought second hand and so own, the renew cycle is nowhere near full. And already people are talking about a new phone. The current iPhone 6 is pretty amazing engineering. They are seeing the largest ever Android switcher rate (read maybe Samsung?), the company still has the highest loyalty rate.

The International Data Corporation (IDC) suggests a smartphone market growing from 1.4 billion units last year to 1.9 billion in 2019, there are still many people out there without the product. In China LTE penetration is only 12 percent. Consumption is happening in China, on the conference call Tim Cook said that McKinsey is projecting that middle class China is going to grow from 14 percent in 2012 to 54 percent in 2022. Plenty of opportunities and room to grow in that part of the world, it will in time be their single biggest territory by quite some margin.

Plus, there are a whole multitude of new products coming, apparently the company is working on a motor vehicle project codenamed Titan. Yes, really. Recently chief of global quality at Fiat, Doug Betts joined Apple in Operations. The Watch I think has just scratched the surface, there are many uses for it. The Mac continues to make slow headway, whilst tablet sales are falling, the company is starting to sell strongly into the corporate market.

The stock is mooted to open at around 122 Dollar, down nearly 8 percent from the open yesterday morning. Not good. Don't stress however, the fundamentals are still really good. They are still set to grow, notwithstanding their big size, at around 13-15 percent in earnings over the next couple of years. Ex cash the stock trades at a discount to the rest of the market, less than 10 times earnings and with a more than two percent yield. Whilst too much of size and scale becomes a problem in time, I think we are nowhere near that yet. We continue to recommend Apple at current levels and see plenty of upside, relative to the rest of the market. Buy.

Linkfest, lap it up

Driverless cars will be part of our future at some point, the question is when and how much automation do the cars have? - Researchers just opened a fake city in Michigan that's the size of 24 football fields to test driverless cars. Testing different scenarios has to be an element to ensure that they are safe and to have the data to show consumers that they are safe.

Given the current theme of commodity prices and gold, here is a piece from one of our favourite bloggers - A History of Gold Returns

Home again, home again, jiggety-jog. Markets have started lower here today, pain across the resources stocks again sadly. BHP Billiton issued a good production report, sadly the selling prices are a whole lot weaker and that is hardly going to change any time soon, I think. Greece votes today again, to rush through everything to get some more money. More earnings today, they are coming thick and fast.

Sent to you by the Vestacters, Sasha, Michael, Byron and Paul.

Follow Sasha, Byron and Michael on Twitter

087 985 093

No comments:

Post a Comment