"Wow, that was exceptionally quick. It seems that the Al Noor and Mediclinic guys worked feverishly to thwart the NMC Health advances announced Friday. This morning there is an announcement that Mediclinic will effectively gain a main board listing on the LSE if this deal would go ahead, and such would be the size and scale of the merged companies that it would be a FTSE 100 constituent, true story."

To market to market to buy a fat pig. It was, at least on the local front, all about SABMiller. And of course more on the money, the AB InBev offer of 44 pounds a share, with an alternative of cash and shares, that equals around 39 Pounds a share. Which kind of explains why the share price of SABMiller settled at 39.33 Pounds by the close last evening, the discount represents both time value of money (these deals may take 9-12 months to close) and uncertainty due to regulatory issues in many different territories. What is evident is that a separate secondary listing will take place here in South Africa, on the local bourse. So you will NOT lose access to this company, you will be able to invest in a larger conglomerate.

Countries that encourage investment and are open to flows in and out are more successful in the long run. I am afraid that as a result of our past we are stuck on this idea that state intervention in the economy is the way forward. It is not surprising that countries like Brazil, India, Russia and China are also stuck in the exchange control mindset. If you want investors locally to be open to all ideas, then exchange controls (which have been relaxed over time) should go.

The ability to be able to send money wherever in the world you want will make your investment choices more, for all the people of the country. Making you more efficient and forcing you to become more "worldly" and by extension more productive. The investible world does not end at the four corners of South Africa, contrary to popular belief. Take a look at this ancient piece of dark history, a passport from the mid 1980's, with a travel allowance amount, stamped in your passport. In theory the restrictions are few for all investors, it is a costly exercise to move small sums of money across the globe. Having global investments however makes you more flexible.

{kind=link}

Off the topic, back to the 9.97 percent move in the SABMiller share price yesterday, which caused the overall market to rise 0.58 percent and now we are above 53 thousand points. The dates are short, we should know by the end of the month what the deal is, it seems that with support of the two main shareholders that should not be a problem. And like we have said a few times, the break fee of 3 billion Dollars, payable by AB InBev to SABMiller is a sign that their internal investigations reveal that they are confident that they will succeed. I am afraid that bar for a few companies that have European exposure (and the UK), all the rest of the top 40 stocks were down. Glencore, at least the share price, continues to be really volatile.

There were results yesterday from Pick n Pay, the market "liked" them, after the trading update was negatively received a short while back. There is still a lot to do for the company, in order to justify that valuation, we continue to accumulate Woolworths as our preferred company operating in that segment. Strictly speaking Woolies are not an out and out competitor, they operate in similar spaces. You could argue that Shoprite Checkers are a more worthy competitor in terms of comparisons.

Taste Holdings reported 6 months results, it has been tough going in the transition from being the franchise controller to now being the business that will operate a whole lot of Domino's and Starbucks outlets, They have the energy and smarts in order to do that, the market is expecting big things. What is very interesting about their business is that the less talked about jewellery business (Arthur Kaplan and NWJ) is growing strongly, that tells you that whilst most will tell you that Joe Consumer is "under pressure", there is still buying of fine items for loved ones. Having acquired Arthur Kaplan, Taste now is the leading retailer by outlets of luxury Swiss watch brands in South Africa. The company is also embarking on a 226 million Rand rights issue to roll out Starbucks (the first 12 to 15 stores will cost 108 million Rand!) and to roll out more premium watch and jewellery stores. These are both premium offerings, which suggests that having done their analysis, the company thinks that middle and upper middle income folks are going to be just fine over the next half a decade at least.

Over the seas and far away, in New York, New York stocks sank in the second half of the session after gains earned in the middle of the session. The S&P 500 dropped around two-thirds of a percent, the nerds of NASDAQ sank 0.87 percent, whilst blue chips lost just a little less than three-tenths of a percent. Across in Asia, the same concerns that weak German and Chinese industrial data points to a weaker global picture. Which then translates to a US Fed that can stay put at this juncture, although much of the housing and labour data suggests that they should act shortly. They really should, just to get the first one out of the way and get some first timers less jittery and used to the idea that rates do in fact go up and down. Remembering that whilst we have seen many programs from the Federal Reserve, bond buying, operation twist and so on, rates have not budged for nearly 7 years. That is a quarter of a generation, a long, long time.

General Electric continues to divest from their financial assets, having agreed to sell their commercial lending and leasing business to Wells Fargo. Believe it or not, even though the size and scale of the book is 32 billion Dollars, and includes 3000 employees, the price has not been disclosed. That is due to the relative size of the seller (GE market cap of 281 billion Dollars) and the acquirer (Wells Fargo market cap of 266 billion Dollars). This is both good news for General Electric shareholders, the company reports on Friday and Wells Fargo who continue to grow their local business, that company actually reports today.

Company corner

As far as we are concerned, the most important company related news yesterday were numbers from Johnson & Johnson. First came the announcement that the company were embarking on a 10 billion Dollar buyback program, which is around 4 percent of the shares in issue at the current share price. This is a sizeable business, not too different in market capitalisation to the two behemoths above, with a market cap of 262 billion Dollars. The business consists of three divisions, a consumer facing business with all the names that you will be familiar with and then the pharma business, with a recently larger and bolted on devices and diagnostics business.

Sometimes, and bear with my whilst I use a cricket analogy, sometimes owning JNJ is like being in Gary Kirsten's camp rather than a dasher like Daryll Cullinan. Gary ended up with more runs and more games than Daryll, it just seemed like poetry flowed from the bat of Daryll. Perhaps a sporting analogy is lost, in this case of JNJ, form is temporary and class is permanent, having lasted 130 years. At the moment, as a shareholder of JNJ over the last 2 years it seems like we have been scratching for runs, the stock is up just shy of 7 percent relative to a market which is up nearly 18 percent over that time. The underperformance has meant that there has been scrutiny placed at the doors of the selectors and coaching staff alike. And by that, I mean us who recommend the stock and management who run the business.

Again, like many multinationals listed in the US and doing business around the world, the strong Dollar has hit revenues, equally however sales in the home base were lower. On an operational basis, adjusted diluted earnings grew 1.2 percent (that is stripping out the currency). In the US the consumer division was all good, unfortunately the other two business segments dragged overall sales lower. On the earnings conference call (you have to signup, it is free however) the medical devices chairman, Gary Pruden, suggested that their division is seeing global growth rates at around 4 percent. And as he points out JNJ are the leader, indeed this as a standalone business would be one of the biggest in the world. He said something that resonated with me:

The World Health Organization estimates that nearly a third of the world's global disease burden could be addressed through surgery. Yet nearly 5 billion people continue to lack access to safe, timely and affordable surgical care.

I spoke to a client the other day who said that her 87 year old husband had a new lease on life with all the replacement parts in his body, and was now able to lead a much more active lifestyle than before. And that is what the diagnostics and devices business is meant to be, with all the technology that abounds (smart devices), it will create longer and healthier experiences for all of us. Having said all of that, adjusted EPS sank to 1.49 Dollars, down 7.5 percent, which is the currency headwinds. Tom Lee, a favourite of the bulls on Wall Street suggested that all these negative Dollar headwinds could unwind to Dollar tail winds in the second quarter next year, I am not a fan of currencies working for or against you, it is what it is however.

So why would you continue to own and even accumulate a business of this size and scale? If you believe that you want to own possibly the bluest of them all, as far as blue chips are concerned, then this is no doubt the company for you. You may consider the company staid and unexciting, yet in the last quarter they spent over 12 percent of revenue on research and development, always searching for the next blockbuster. Changing lives, one at a time. On a historic multiple of over 16 times the stock is not cheap relative to their recent growth rates, the fabulous underpin of the 3.14 percent yield (pre-tax) should put a floor in. Whilst there is no great hurry to buy them before they see the effects of the currency unwind and turn in their favour, this is a company that you must always own. Accumulate on weakness.

Wow, that was exceptionally quick. It seems that the Al Noor and Mediclinic guys worked feverishly to thwart the NMC Health advances announced Friday. This morning there is an announcement that Mediclinic will effectively gain a main board listing on the LSE if this deal would go ahead, and such would be the size and scale of the merged companies that it would be a FTSE 100 constituent, true story. It is not easy to follow, and a little complicated as a result of obtaining the inward listing (again, as a result of exchange controls), the payment of a special dividend to sweeten the deal and raising of money by Remgro in order to achieve this. Remgro will continue to be the anchor shareholder for Mediclinic, they have already indicated that they will vote in favour of the deal, on the Al Noor side the shareholder missing from the equation is the private equity crowd, Ithmar capital who haven't given an irrevocable yet. 28 percent held by Sheikh Mohammed Bin Butti Al Hamed, and 6 percent of Al Noor held by founder and deputy chairman, Dr. Kassem Alom, have agreed to vote in favour.

Quickly, what are the terms here? What would you get as part of a group that would be renamed Mediclinic International Plc? Quite simply, in the new entity you would get 0.625 shares for every one that you hold currently. Here is the announcement: Recommended combination of Mediclinic International Limited and Al Noor Hospitals Group. The combined business revenue split would be as follows, in Dollar terms: 46% from Switzerland, 31% from South Africa and 23% from the UAE. Al Noor, the share price in London is trading currently at 996 pence, the deal price is 8.32 pounds per Al Noor share and a special dividend of 3.28 pounds, effectively 11.60 Pounds, a 16 odd percent premium to where the price is trading right now. And importantly, as the release points out, a 39 percent premium to the 1 October share price, before any deal related activity.

Read it carefully, the important thing to note, as the deal stands right now, this is earnings neutral for Mediclinic and accretive in subsequent years. In terms of the existing shareholders and depending on how much the shareholders of Al Noor are willing to sell to Remgro, Mediclinic shareholders as they exist right now are expected to own around 84 to 93 percent. Shareholder votes on both sides will happen shortly, the combination is expected to be finalised before the year is out and the transaction is expected to happen in the first quarter of next year. That important factor to keep in mind, Al Noor shareholders will be diluted out of sight, you will first get 0.625 shares of Al Noor per Mediclinic share, in the new company that will have access to cheaper funding in order to continue to consolidate the private hospitals space. We endorse and will update you as this goes along, it is a positive for both sets of shareholders.

Linkfest, lap it up

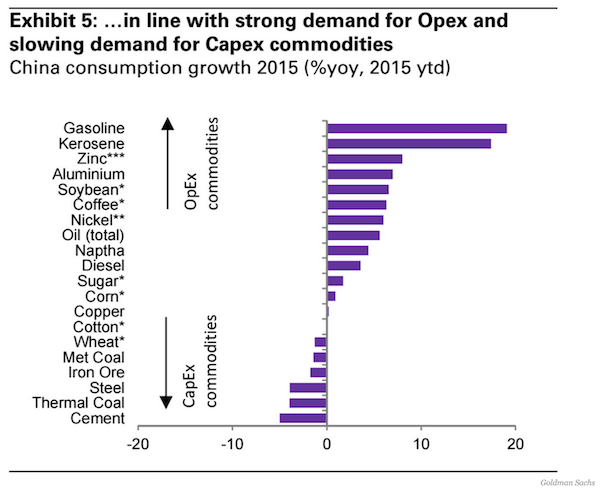

We have all seen the massive drop in commodity prices due to demand slowing in China and increased supply due to efficiencies from the miners. Here is a look at how the Chinese economy is changing gear to more consumption (there are only so many bridges you can build) - One clear chart shows that China's massive economic transformation is working

Hedge funds have received some attention lately with one of the bigger ones doing badly, resulting in them returning cash back to investors and shutting shop. - Why People Invest in Hedge Funds. Here is what the oracle of Omaha thinks about hedge funds - Warren Buffett dumped on hedge funds for a promise that lasts long enough to get them rich. It has been said that hedge funds are "tax on the rich".

The big problem with driverless cars is that you need to program morals into them. Who dies if the choice is driving into a crowd of people or into a tree killing the driver? - A Stanford Professor's Quest to Fix Driverless Cars' Major Flaw

Home again, home again, jiggety-jog. Markets across the East are lower, the economic news has not looked great, the companies news hopefully over the next few weeks will look better than he market anticipates and it will be "business as usual". As we often point out, you only really have to worry (if that is the right word) about your subset of stocks.

Sent to you by Sasha and Michael on behalf of team Vestact.

Follow Sasha, Byron and Michael on Twitter

087 985 0939

No comments:

Post a Comment