"There is an option to take shares, they would however be subject to a five year lockup and they would not be listed on any stock exchange. At the end of the five year period, they would be convertible on a one for one basis to an AB InBev share. If you elect for the part cash and part shares, the ratio is as follows: "SABMiller shareholders who elect for the partial share alternative will receive 0.483969 Restricted Shares and GBP 3.7788 in cash for each SABMiller share." The current share price of AB InBev is 111.49 Dollars. Apply that ratio, and you get to 53.95 Dollars plus 3.7788 Pounds in cash. Or in Rand terms, 720.11 Rand of shares and 77.36 Rand of cash, equalling an amount a fraction short of 800 Rand. Reminder, the share price closed last evening at 732 Rand. If you take the cash offer of 44 pounds, that equals 901.82 Rands a share."

To market to market to buy a fat pig. We often talk about "the market" as if it is a beast of some sort, or if it exists with a mind of its own. We make that mistake from time to time in which we use the S&P 500 as a benchmark for global equities, as we learn from several posts over and over, it is not. This post from Mark J. Perry, which is self explanatory: Fortune 500 firms in 1955 v. 2015; Only 12% remain, thanks to the creative destruction that fuels economic prosperity.

The explanation that Prof Perry gives in the middle of the article is perhaps not what you were expecting, I was however, seeing as I know his work pretty well: "The constant turnover in the Fortune 500 is a positive sign of the dynamism and innovation that characterises a vibrant consumer-oriented market economy, and that dynamic turnover is speeding up in today's hyper-competitive global economy." Do you get what he is trying to say here? He reckons the fact that the company turnover is so high, means that in his mind, innovation and dynamic deal making activity means that the composition of the index is always going to be changing, you would not however expect this much change over a 60 year period. Deals happen, company's merge and change course, go out of business for whatever reason, get smaller as a result of divesting, go private, a whole host of reasons. The market today is definitely not the market of tomorrow.

Company corner

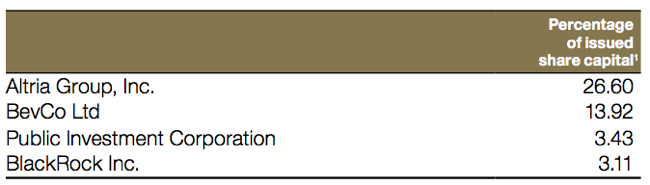

{This was written before the known news!} What is really going on in the minds of the SABMiller board, many pointing out that the kingpin in all of this is the chairman Jan du Plessis. He has only been chairman of the business since 1 September 2014. He is also the chairman of Rio Tinto, and has been so since 2008, thwarting BHP Billiton in the merger of equals, suggesting that the company was undervalued. Or wait, probably it was actually the financial crisis that led BHP Billiton to withdraw their bid nearly a whole year after they announced it initially in November 2007. Back to SABMiller, the shareholders appoint the board to act on their behalf, they voted them in and now I guess would be engaging with this board during this whole process. From what we have heard both the main shareholders, Altria (with nearly 27 percent) and BevCo (the Santo Domingo family, with nearly 14 percent of the shares) have apparently been leaning towards this deal.

Yesterday there was a another offer on the table by AB InBev, still not at the 44 pound Sterling mark that would crack this deal. So why does and why is the SABMiller share price trading at 36.67 Pounds? It is still a long way away from any price put on the table, or rumoured price. If the SABMiller board are really on the same page as the PIC and think that this deal significantly undervalues the company, then why isn't the share price trading closer to that? Before AB InBev came along, the share price was trading below 30 pounds a share, admittedly in a depressed market. Let us presume that the stock had recovered in the August wash out, it is fair to suggest that it would be trading around 32-33 pounds, and could be around 10-15 percent lower than it is currently. What would it take then to move the share price higher, to the 43-44 Pounds where AB InBev is hovering currently?

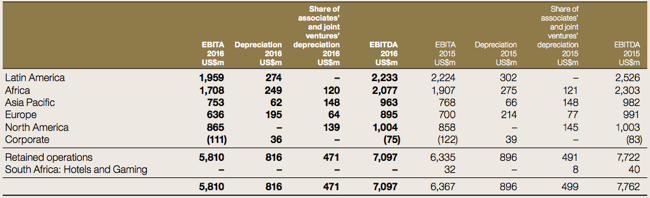

Even if the company garnered a, let us say 23 multiple, as a "growth stock" in emerging markets, along with their developed market exposure, what earnings would they need in order to get there? Working backwards, around 1.91 pounds worth of earnings, which is a full 58 cents higher than the last financial year. Or another 43 percent higher in earnings from here. Given that this (as per the last annual report) has been the growth rates in EBITA:

It may take another four to five years to reach that 1.91 Pound earnings mark, and as such at a 23 odd multiple, that would be the next time that the share price got to that level on a "normalised" basis. Now there are so many moving parts in here that it makes charging the flux capacitor easy. My drift is that if AB InBev is thwarted by Jan du Plessis and the rest of the board, are shareholders happy to wait until 2019, 2020 to see the share price get back to that sort of level? What has Alan Clark got to gain if this deal happens? A lot it seems.

If you look at page 96 of the last annual report, you can see that he had outstanding options of 1,249,168, having seen 715,401 options vested and exercisable as at the same date. Equally, he owned at the end of the period 298,764 shares in total. Doing simple math, a deal at 44 pounds a share would net Alan Clark 13 million pounds on his shares free and clear, not to mention the gains on the options that have vested.

Big numbers we are talking, even more eye popping when you consider the number in Rand terms. We are talking nearly 270 million Rand, just on the shares free and clear, holy smokes. I have not done the math on the share options, are we talking somewhere in the region of 700 odd million Rand. Surely not, for a corporate job of leading a company that sells beer, with ten years of options? Does that sound egregious, or is it just par for the course?

So at the same time you must consider that the board, and el chiefo himself has loads to gain if a deal of this nature does happen. And I am pretty sure that he can happily spend more time with his money, as can the rest of the board. As we have said over and over again however, it surely must matter more what the top shareholders say, here they are, we already know that the PIC have said no, possibly for exchange control issues alone:

There is nothing really to do at this juncture, the share price tells you that Mr. Market is sceptical of a deal at this point. If that was and is the case by the close of business tomorrow London time, then there are two things to watch, firstly, what recourse will the shareholders have, most especially if the largest ones wanted a deal and secondly and more importantly, to what level will the share price fall if a bid falls away. Most especially against the backdrop of average volume growth numbers recently and measured (in quarts if you want) growth in emerging markets, the strength of the company. Let us watch it!

Wait. As this is a fluid situation we get to update it in the middle of writing. It seems like, as per the website: SABMiller and AB InBev agreement in principle and extension of PUSU deadline. Ha-ha, all the writing that I have just done above was speculation. I guess that a deal is not a deal until the money is in the till, as they say in the classics. As you can see, there is a partial share alternative, which should please the PIC. There is a whopping 3 billion Dollar break fee.

There is an option to take shares, they would however be subject to a five year lockup and they would not be listed on any stock exchange. At the end of the five year period, they would be convertible on a one for one basis to an AB InBev share. If you elect for the part cash and part shares, the ratio is as follows: "SABMiller shareholders who elect for the partial share alternative will receive 0.483969 Restricted Shares and GBP 3.7788 in cash for each SABMiller share." The current share price of AB InBev is 111.49 Dollars. Apply that ratio, and you get to 53.95 Dollars plus 3.7788 Pounds in cash. Or in Rand terms, 720.11 Rand of shares and 77.36 Rand of cash, equalling an amount a fraction short of 800 Rand. Reminder, the share price closed last evening at 732 Rand. If you take the cash offer of 44 pounds, that equals 901.82 Rands a share. It is in the short term more advisable to take the cash, what the share price trades at today however, would reflect reality in-between of the blended option.

Not a done deal, closer to the end of the road and now presenting a titan that would sell around one third of all the beer in the world. AB InBev are that confident to present a large break fee, equally the shareholders of SABMiller are taking the lock up shares and partial cash, slicing some of their investment off (mind you, that is probably more than they got the shares for in the first place, when those respective deals happened). As Warren Buffett always said, you should be willing to own something on the basis that the market closed tomorrow for five years, for Altria and BevCo this is about to become a reality if all the conditions are met.

Linkfest, lap it up

Welcome to the future. The technology is still wildly expensive but will come down with time as production numbers increase and as technology gets better - A Prosthetic Arm That Gives Amputees the Sense of Touch

What are your returns likely to be going forward?Probably anything except the average return in the market - Annual Stock Market Returns. Here is why a long term buy and hold strategy has worked, assuming that you hold quality - "Of the forty years when the Dow was negative, the average return was -15.3%. What's important to understand is that a 15.3% gain does not negate a 15.3% loss. A decline of 15.3% requires a 18.1% gain to break even. The good news is that the average positive return is 19.4%."

Take this quick quiz and see if reality meets perception - A quick puzzle to tell whether you know what people are thinking. The scenario illustrates what is called the "majority illusion", where people who are in the majority on certain views think they are the minority. The reason? The people in the minority make more noise and connect with more people, thus creating the illusion that their view is in the majority. A good example is the news that we read everyday, only picking the outrageous things to write/read about means that your "reality" becomes the idea that the world around you is falling apart and outrageous.

The Nobel prize in economics was announced yesterday, here are some interesting facts about the Scotsman who now lives in the US - Nobel Prize Winner Angus Deaton Wrote the Book on Inequality Before Piketty.

Home again, home again, jiggety-jog. SABMiller has opened nearly 11 percent higher. Nowhere near the cash price, closer to the shares and cash price, perhaps telling us that this is by no means a done deal, nor is it all totally cash. That second part we know. As a result of that monster move from one of the biggest listed companies on the exchange, the resources complex quite a bit lower is making sure that the balance of the market is not significantly higher.

Sent to you by Sasha and Michael on behalf of team Vestact.

Follow Sasha, Byron and Michael on Twitter

087 985 0939

No comments:

Post a Comment