Jozi, Jozi 26o 12' 16" S, 28o 2' 44" E. Locally we were watching the Medium Term Budget Speech, although not giving it our complete attention. I did however give it more attention a little later in the day and read through most of the document titled: Medium Term Budget Policy Statement. Moneyweb traditionally always do a good job of the budget, check out the lead in that segment: This is not an austerity budget.

I guess the most important thing from where I sit is that the folks in this country that advocate fiscal discipline were the people that heaved a sigh of relief. And some folks of a bearish nature said, that is very nice, but implementing this will be the harder part. But like most things in life, I suspect that a little direction pointing can be achieved if you have the will. I am still always amazed that education and health get such a high allocation of the budget, but yet we seemingly are not making progress in those critical areas.

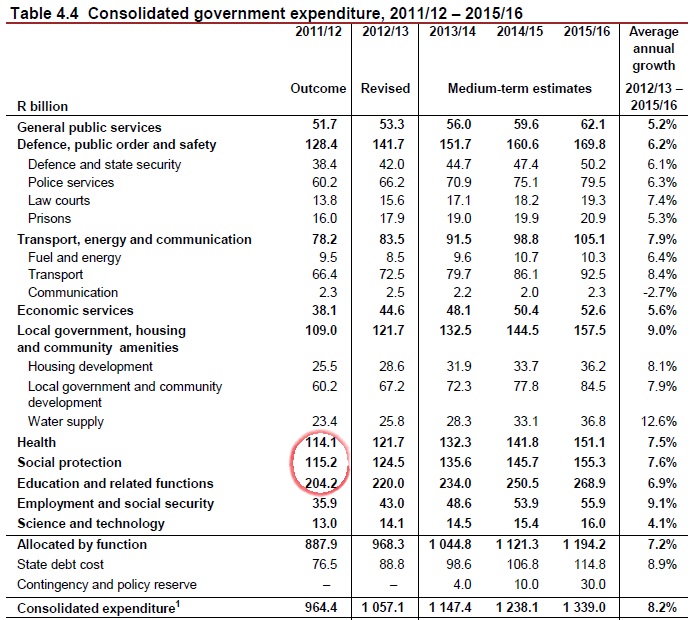

Check this out though. Here is a table hacked from the above download. It is possibly the most important thing about this budget for me.

If you add those three allocations up, the ones that I have circled, health, social protection and Education and related functions, you will be quite astounded. Before servicing debt, as a percentage of the overall allocation, those three (critical to our future) departments account for 48.8 percent expenditure. Nearly half. And if you Google South African Education, you come across articles like this one: SA education a sinking ship - Ramphele. And when you Google South African health care, you come across articles like this, from the same publication: SA plans to cure sick health system.

So, we have the resources. We allocate them accordingly to the relevant departments. It is the management thereof that makes all the difference. I for one would like folks like Prof. Jonathan Jansen running the basic education department. I suspect that the incumbent, Dr Aaron Motsoaledi is very well intentioned and is the best man for the job. Some of the commentary that he makes about private healthcare I do not agree with. After all, private schools and private healthcare would cease to exist if the public version was up to scratch. Perhaps there is a lesson in that. Give Curro Holdings government money to run schools, some problem schools and see if they can get by and deliver on that budget. Get Netcare, Life Healthcare or Mediclinic to run government hospitals and see if they can do a better job. I suspect that they would. Would it happen? No ways. Refer to the conclusion of the Telkom piece below.

Cynthia Carroll has decided enough is enough, and she is stepping down from Anglo American as CEO. The release is on the Anglo website, you can read the full announcement here: Cynthia Carroll to step down as Chief Executive of Anglo American. The response from twitter was, well that was about time, and at last. Not, she will be missed and what a loss for the company. Chairman John Parker was a little more flattering: "Cynthia's leadership has had a transformational impact on Anglo American. She developed a clear strategy, based on a highly attractive range of core commodities, and created a strong and unified culture and a streamlined organisation with a focus on operational performance."

I guess it is easy to blame mistakes on an individual and not the board as a whole, but some decisions are going to be remembered more than others. From their 2008 results the company bought back 1.7 billion Dollars worth of shares, out of the 4 billion Dollars proposed. Shareholders would have voted on that. There was a previous buyback program before Carroll arrived, where the company bought back 2 billion Dollars worth of shares, that was back in 2006: AA plc Share Buyback Programme 1. So perhaps it is not entirely fair to say that it was all her fault. But she drove the bus, when almost each and every day through 2008 all the way to October 3 2008, share buybacks were being announced and taking place. Blame everyone, including the shareholders that approved the buybacks.

But there are some specific projects that she can be "blamed" for. Minas Rio. Again, the board agreed and shareholders would have approved. With regards to safety, I suspect that this is probably something that she can be apportioned blame. Plus, the handling of the copper assets in South America, in Chile and the high profile fight with Chilean government copper company Codelco, that seemed just downright embarrassing at the time. Oh, and remember she was at the helm when Anglo American passed on the dividend for the first time since World War Two. Not anyone else, but her.

The job for the next person will be tough. There will be the same old issues around mining in South Africa. Will the next person be bold and cut, slice and dice! Different divisions would perhaps be given a higher valuation. Maybe. Well, let us not speculate. What Mr. Market does like, however, is that she is leaving. The stock is up two percent in London, to 1896 pence. From the beginning of March 2007 to yesterday, the stock is down one third in London. Thanks Cynthia. Over the same time frame BHP Billiton is up nearly 77 percent. Rio Tinto is up 5 percent. Xstrata, you could have done worse, is down 63 percent. The FTSE is down 5.5 percent. Yip, the Anglo share price has comfortably underperformed even the index. The CIO of the PIC (5.58 percent shareholder), Dan Matjila, was quoted by Bloomberg saying "The performance was more about poor decision making than it was about tough markets.". Check out the Bloomberg story: Anglo's Carroll Quits as First Woman CEO as Miner Lags

OK I know that it is news from a couple of days ago, but it is worth pointing out. The Telkom AGM went, how should we say, more than a little badly for a few directors hoping to be re-elected. The circumstances were more than a little bizarre though, I was following Moneyweb journo Monique Vanek on Twitter, who was there, at the AGM. In a twist, it seems like government, through minister Pule, changed their vote and ousted four non-execs. Including Sibusiso Luthuli, who was supposed to assume the the chairman role, after current chairman Lazarus Zim had indicated he is out of there. Check out Vanek's updated story: Telkom board members ousted, government shows its hand.

Now I have no idea what the agenda is of the state, perhaps it is even a cost cutting exercise and the company does not need such a big board, but someone on twitter suggested that three of the four were chartered accountants. I checked this out, true, Luthuli, Waja, Mnxasana are all chartered accountants. And Sibisi (sorry, Dr. Sibisi) has a PhD from the Department of Applied Mathematics and Theoretical Physics (DAMTP), Cambridge University in 1983. Source -> Dr Sibusiso Sibisi. So I decided to look at the rest of the Telkom board, who was left behind. And you know what, all really qualified, you can check what board members remain by seeing who they are in the Telkom 2012 Annual report.

So it leads me to the same thing that I have been saying over and over again, the meddling of the main shareholder in the business has held the place back. Too much control by labour too. As we said here in the office yesterday, Telkom property, plant and equipment (their fixed assets) is valued at 36.155 billion Rands on their balance sheet. But yet Mr. Market values the company at 9.348 billion Rands, as at last evenings close. So clearly the company is more valuable than we think, but the earnings are not exactly there to justify a higher rating. If government ever got tired and threw in the towel (I doubt it) then someone would have to pay a (very hefty) premium on the current price to get government to change their mind. I for one would see MWeb doing a much better job of sweating these assets a lot more, but hey, I don't wear a little black cap and I don't carry a little red book. Plus I don't have a little Lenin's beard. So I think differently to people who embrace that appearance.

- Byron's beats

Yesterday Amazon reported its first loss for a quarter in 9 years as the company continues to invest in the future at the expense of current earnings. Net sales increased 27% to $13.81bn compared to $10.88bn this quarter last year. Because earnings have been scarce, sales have been the main gauge of growth for this company so this figure is important to note. The operating loss equated to $28 million compared to the $79 million profit made last quarter. This equated to 60c a share.

It is hard to value a company like this because it is so focused on growth. Which of course is a good thing as an investor of a specific kind. A good operator should not worry about a share price in the short term. Big spending was done this quarter with 2 new massive warehouses being built in Los Angeles and San Francisco. This was done with a goal of same day deliveries in mind. On top of that they are selling their signature product, the Kindle Fire at breakeven in order to lock in clients.

With that said analysts expect earnings to come in at a measly $1.86 in 2013. I say measly because the stock trades at $222. But expectations are for this year to be the absolute bottom of margins. Forecasts for 2014 see earnings coming in at around $5 a share, a huge jump from the year before.

For me, and I know its unconventional, I feel you need to get a feel for this company and without looking at the numbers, logically assess whether this company is going print money in a few years time. I am an Amazon customer, I love buying books from their site and reading it on my iPad via the Kindle app. Reading is never going to go out of fashion and the convenience of ebooks is a winning business model. Amazon have first mover advantage here with most publishers committed to their site. Even if they do take 70% of the sale price (I heard this from someone who researched selling his book on the site). Wow that is huge.

Online retailing is huge. As a South African who is fairly technology astute it is fast becoming a way of life. Judging by the stats I have read, in the US it already is. In a huge way. But it is a fickle business. Clients want trust and efficiency. On the day deliveries and a very sophisticated payment system will maintain Amazon's position here. I am not too worried about current earnings. Steve Bezos is very impressive. He reminds of Steve Jobs, passionate and not fazed by criticism from impatient investors. It is not for everyone though, doesn't expect dividends anytime soon and patience is needed. Coming from our fairly conservative approach, I would call it a hold.

Apple missed expectations last evening, the company reported Fourth Quarter Results after the bell. A record September quarter, with revenue of 36 billion Dollars and profits of 8.2 billion Dollars, which in turn translated to basic earnings per share of 8.76 Dollars. A dividend of 2.65 Dollars per share was declared. Revenues were ahead of expectations, iPhone sales were ahead of expectations at 26.9 million units. That was an increase of 58 percent over the corresponding quarter last year. That is huge, but the shareholders expect that, huge increases. iPad sales on the other hand fell light of expectations. Some folks are saying that the iPad miss is more than just a little disappointing. And the mini, what does it mean for those sales when the pricing is quite aggressive. Mac sales, Paul got one the other day, also set a record meaning that the migration across to the laptop from more traditional places has happened too. Once people get used to the quality, they want Apple in all of their hardware.

Costs are an issue for the company, profit margins are lower than in previous years with heightened competition from the likes of Microsoft and Amazon. Perhaps, having seen Samsung results this morning, that is the one who is competing on price and product, Amazon you saw above are not exactly munching Apple to pieces. I saw a note the other day that suggested that Apple had quickened their product pipeline release to every six months from every year. So, perhaps the allure of the stock and product combined will not exist as it had before. Has the company really lost their mojo? Well, I suspect not for the time being, their products are still amazing. I own an iPad, an iPhone and recently Apple TV was an addition, I am getting close to completely figuring that one out. So far it has not received all of my time and effort.

On the conference call CEO Tim Cook and CFO Peter Oppenheimer spoke of 700,000 applications on the Apple iStore, of which one quarter of a million were for the iPad, or compliable with the iPad. Also, what we knew but what was confirmed was that demand currently outstripped supply for the newest Apple iPhone, the iPhone 5. That said, the iPhone 5 is going to be rolled out across 100 countries faster than any other iPhone release ever. Tim Cook said in the release: "We're entering this holiday season with the best iPhone, iPad, Mac and iPod products ever, and we remain very confident in our new product pipeline."

That is ultimately the "thing" that will drive Apple higher in the coming years, new product pipeline. People have gone to sleep on the whole idea of Apple iTV (not to be confused with the set top box), which was a big new wow product that was seemingly coming. Adoption by enterprise is important, most Fortune 500 companies are testing or using iPads across their business. And this was supposed to be a tool that would only "work" in the home. I didn't read the report and come away feeling disappointed. The fact that the company has had two quarters of missing expectations, that is an issue for the anxious. I suspect that in the coming years that Apple will continue to attract a wider fan base. The phone still is in part a fashion accessory. No really, people want to own the phone.

I suspect that this earnings report has highlighted that the company is not immune to supply chain disruptions (people at Foxconn want to earn more) and competition from their peers, who have closed the gap. Apple set the benchmark, everyone else wants to beat that. This is good news for innovation. I maintain that whilst the short term outlook has been clouded and questions have been asked about continuing Steve Jobs legacy at Apple, the stock is still a buy at current levels. We always said that this was a company and investment that you would have to watch closer than most. As the WSJ points out, their closest competitor is also feeling the heat after a record quarter: Samsung's Success Is Its Biggest Weakness. Most people I speak to want the new Galaxy or the new iPhone. I guess until that changes, times will be tough for Nokia, RIM and their competitors, Google has great aspirations here, they are the third competitor. Microsoft are the dark horse here too. Competition is good for innovation.

Crow's nest. US GDP will be a huge number ahead of the election in less than two weeks time. I suppose that Jack Welch has his own ideas about that release, perhaps the Chicago "guys" will do something to juice it up. Until then, we are lower to start with!

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment