Jozi, Jozi 26o 12' 16" S, 28o 2' 44" E. It could have been worse, it could have been better on Friday, but I guess we were "saved" by a better than anticipated US GDP read that had a 2 at the front. 2 percent growth exactly is what the advance estimate for the third quarter presented Mr. Market, confounding a few folks no doubt. As the release said however: "The Bureau emphasized that the third-quarter advance estimate released today is based on source data that are incomplete or subject to further revision by the source agency." So it may be those Chicago guys again I said, referring to the Jack Welch remark, perhaps the insinuations of which were not the most palatable comments ever made. Thanks Jack, but everything is not sooooo bad. Just worse than you would have hoped. Or perhaps ironically in his case, he would have hoped for poor economic data so that his fellow (Romney) could get elected. Because then Romney could put things right, at least in the mind of the republican faithful. Hey, we don't have to wait too long for the results to be in, around two weeks or so.

Markets trended higher through the afternoon, but we were unable to end in the green. Industrials, retailers and gold miners all sank over a percent, the platinum miners actually added half a percent. On our screens this morning are pictures of a London Based Bloomberg reporter, Olivia Sterns witnessing and reporting on workers at Rustenburg just yesterday taunting police. Just a few days after what seems a visit to Botswana where she was impressed with the De Beers mine there. These are the pictures that the world sees of us. Sad, but true. But don't get down on yourself, read Peter Bruce's "thick end of the wedge" column in BusinessDay this morning: The Publisher's Notebook. Keep calm and carry on, it seems. In the moment it is easy to feel beat up. But. But. Bruce's first love is sport, or seemingly so to me at least, which he gets too emotional about. Like most sports fans they can't understand why their team just can't win every weekend. Quite.

Nedbank released a trading update this morning, at face value it all looks fine to me. The group points out that the operating environment is tough, European economies are still under pressure, and emerging markets are experiencing slower growth. No de-coupling, remember that? But they are still on track to meet their earnings growth targets for 2012. Net interest income grew 9.2 percent, net interest margins actually grew to 3.5 percent. Non-interest revenue actually grew 13.9 percent. Which is not always a good thing (penalties and fees), but they break it down, pointing out that trading income increased a whopping 28.3 percent. I shall have to dig a little further there.

It was not the actual trading update which looked just fine to me, but rather the muted outlook, which is a little clouded: "Given the prevailing economic slowdown and uncertainty combined with the effects of wage related strike actions, the group remains cautious on its outlook." Cautious, but that has been the watchword for a while in fact. But I want to make one last point, which I do make from time to time. Many folks stress about unsecured lending in South Africa. Nedbank total advances grew 6.8 percent to 521 billion Rands.

That is a big number, not so? But hear me out here, just last week the Reserve Bank said that unsecured lending had jumped a whopping 21 percent to 43 billion Dollars. At the current exchange rate of 8.66 ZAR to the USD that is 372.4 billion ZAR. Which is a monster number, but it is "only" 71.4 percent of the entire Nedbank loan book. So who is the unsecured lending going to? And make no mistake, Nedbank are in the business of unsecured lending themselves, it is a profitable business. I suspect that the businesses suffering the most are the folks that fall into the poorly regulated category. Perhaps I am being naive, but I suspect that the best systems are owned by the best businesses in the sector. But I am not trying to poo-poo the issues surrounding the sector, South Africans are under pressure, specifically the target markets for the unsecured lenders. But who is the target market? Ironically it can be almost anyone. In weeks from now we will see a trading update (maybe) and numbers from the biggest lender in that space, African Bank. They are of course a September year end.

Oh, my last observation was on the Nedbank deposit base, which grew by 8.6 percent to 555 billion Rands. Why? Well, Nedbank indicate that they have been working hard to build and enhance their deposit base, but so has everyone. I guess the issues around reluctance to invest, in light of a patchy outlook remains. What I would like to see, and we are only going to get a sense of this next year when all the banks report, is what are business deposits looking like? Are businesses borrowing less and saving more? I suspect that might well be the case.

Mediclinic released a trading update on Friday afternoon. It is an investment theme that we like a lot, healthcare. The thinking is pretty simple, the richer people get, the longer they are inclined to live and spend on their health. The Americans on a per capita basis still spend the most on healthcare, the benefactors being big pharma, medical professionals and perhaps the "wrong" quarters. Mediclinic has a business in Switzerland, where on a per capita basis the country ranks third globally, at around 5200 USD per person. For perspective, we spend about the same amount as Turkey, Mexico and Brazil on healthcare. The further down the global list you go, unfortunately you see the familiar "faces", with Eritrea at the bottom, spending a mere 18 Dollars per annum per person. Population there is around 6.1 million folks. In Switzerland, there are roughly 8 million people living there. Yet in Switzerland, the average spend on healthcare is 290 times above that in Eritrea, on a per capita basis. Unfair I guess you could say, but that is the truth. Divergent histories and wealth creation over time I guess, using the resources available.

That is one of the reasons why healthcare is such an emotive issue, people will argue that one life is not worth more than another. It turns out that the truth is much uglier than that. What was not ugly however was the trading statement from the hospital group, that operates locally, in Dubai and in Switzerland. A few in Namibia too, three is a few, not so? The share price has gone bananas (which are good for you, full of potassium), over the last year the stock is up nearly 27 percent. Very good! Five years, a more modest 95 percent growth, which is also awesome. The earnings are expected (without the once offs which include currency translations) to be between 40 to 50 percent higher than the corresponding period. This is for the half year to end September. Excellent, well done chaps! We still have concerns about the hospital groups in South Africa, government is still very combative towards these businesses, which have done remarkably well. Results are expected late Tuesday or early Wednesday next week.

When you look at it at face value, Shoprite sales for the first quarter of their financial year are on fire! The company had an operational update this morning, and the numbers don't quite take your breath away, but given the ropey looking outlook delivered by many retailers out there, this looks good. The group refers to depressed market conditions. Total group turnover increased by 15.6 percent, boosted somewhat by a weakening Rand. In their core business, in South Africa, sales grew 12.2 percent, internal inflation has softened to 3.6 percent when compared to the 4 percent for the corresponding three months. But listen to this, in constant currencies their African business grew sales 26.4 percent. In Rand terms, because of the weakening currency, sales increased a whopping 34.3 percent. As they say, the comparative quarter saw growth of only 12.7 percent. If you were looking for a reason why the stock trades on nearly 30 times earnings, here it is above you. Some would say that you are nuts to pay that for a retailer, but the base is low on Africa and there are not too many choices at this size and scale. So, regardless of what you think, this is what longer dated investors think. They should trade on higher multiples.

- Byron's beats

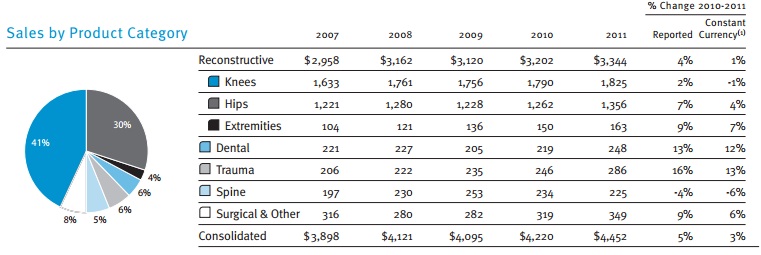

Here at Vestact we have four big investment themes namely aspirational consumers, commodities, technology and healthcare. Within the healthcare sphere we have Aspen and Discovery locally and predominantly Johnson & Johnson in New York. However we also have a couple of smaller companies with exciting prospects over in New York, the options there are endless. One of those is an $11bn market cap company who specialises in joint replacements called Zimmer Holdings. Here is a brief description from the company's website.

"Founded in 1927 and headquartered in Warsaw, Indiana, Zimmer designs, develops, manufactures and markets orthopaedic reconstructive, spinal and trauma devices, dental implants, and related surgical products. Zimmer has operations in more than 25 countries around the world and sells products in more than 100 countries. Zimmer's 2011 sales were approximately $4.5 billion. The Company is supported by the efforts of more than 8,500 employees worldwide."

To get an even better idea of what they do I have hacked a table from their 2011 annual report which segments sales by category.

Zimmer released 3rd quarter results on Friday which had earnings come in slightly above expectations. Let's look at the numbers first and then analyze how the company looks as an investment prospect.

Net sales for the quarter reached $1.026bn which was down slightly due to currency adjustments. Adjusted earnings per share came in at $1.15 vs estimates of $1.13 which was up 10.6% from this quarter last year. Estimates for the full year 2012 (these are usually quite accurate because we already know 3 quarters) are for around $5.27. Trading at $63.55 the stock trades on forward 2012 earnings of 12 and forward 2013 earnings estimates ($5.70) of 11.2.

As you can see growth is not expected to blow the lights out. That is because most of their products rely on elective procedures. When times are tough, especially in the likes of Europe (where 27% of sales come from) elective surgery is usually delayed. But we remain optimistic. 55% of sales come from the US which is an economy showing strong signs of growth. If your home is worth 15% more than last year you are going to have more of an incentive to splash out on that knee replacement you have been needing for years. And it literally changes lives.

Imagine how many bad hips and damaged knees there are in the developing countries. 18% of sales come from Asia Pacific and as these people become richer and older, life changing surgery will surely be prioritised. We continue to add to the stock. Not only does it look attractive at these levels but because of its size it presents itself as a potential takeover target in an industry where M&A activity has been fairly high.

Digest these links.

You might have heard us beating on this drum that mobile markets are anything but mature, perhaps voice is, but data (which is lower margin) is a long, long way away from being anything that resembles mature. In fact, in an African sense it is almost Jurassic. Last week, if you recall when we saw the MTN subscriber release, there was talk about the 2G network in Nigeria. Here in South Africa, in the urban areas we are getting excited about the prospects of 4G/LTE coming in days that you can count on less than a families hands and toes. Even less than that! Well, then I guess that you wont be too surprised to read this: Angels in Lagos. It is small, laughably small in fact, the Lagos version of what is Silicon Valley will need a whole lot of luck. But cheaper smartphone adoption, improving network speeds and a hungry public mean that they have all the right ingredients. On the East Coast of Africa I saw an interview with a mobile guy on CNBC Africa in which he said that Africa did not have the same problem around getting users to adopt mobile, users in fact knew no different, the fixed line infrastructure was poor and outside of the urban areas generally unavailable.

OK, the news in, in the wee hours of Monday morning, late evening Sunday in New York, was that hurricane Sandy had struck a blow for socialism and had succeeded in persuading the NYSE to close up shop on Monday. Earlier the NYSE had agreed to just let the electronic trade take place, but on further consultation had decided to shut the whole lot down. Thanks hurricane Sandy. I have friends in New York, who are celebrating a birthday (a milestone), I am not too sure when they were supposed to come home, but that is a pretty poor showing for them. I quite liked this unusual post: The Subway Looks Kind of Creepy When It's Empty.

I am not one for charts. I believe that looking at something that has happened and trying to suggest that the same will happen is just plain stupid. A chart shows interesting historical information and gives you context. But that is about it. So that is why this post: P/E Level For S&P 500 Index At Level Not Seen Since 1990s should be seen in the light that perhaps investors have shifted their goal posts to reflect less certainty. In fact I am pretty sure that this is the case. Investors are not willing to pay more for equities, than in 1990 when most middle income families saw a personal computer as a luxury. My dad was perhaps by South African standards an early adopter, we had a Commodore 64. Remember those? The market was about as cheap back then as it is now, the late 80's, early 90's. And that was when the iron curtain still existed, even if it was showing signs of cracking. What does this mean? Nothing and something. Nothing to those burnt twice in the last decade. Something to longer dated investors. Price is what you pay, value is what you get, is that old Buffett quote.

So then, why is US consumer confidence at the highest levels in five years? Consumer sentiment at highest in five years in October. As the article does point out however, the clouds on the horizon could be the fiscal cliff, but at least every man and his dog is aware of that! Some are starting to even suggest that it would go a long way to lowering the debt to GDP outlook over the long run. All that matters to me is the growth rate. If that increases, the debt issues will take care of themselves.

Crow's nest. Today sucks in one regard. It is the end of the daylight savings in Europe, the clocks were turned back an hour over the weekend. The same happens in the US next weekend. Why does this suck? Because we effectively "lose" an hour of synchronised trade with Europe, they will now start an hour later than ourselves for roughly six months. The US one is worse, because instead of us starting at 15:30 alongside their markets, we effectively only get half an hour. The futures market of course keeps us in check and balance. That said, the US is closed today, Sandy has seen to that. I said to my daughter this morning, expect Patrick at some stage, but you are never going to see SpongeBob. Hurricane SpongeBob, you would think that would be drier than most. For the time being our markets have started a little lower here today.

This is a huge week. Jobs week for starters, US presidential elections are close, as is the Chinese transfer of power internally in the Communist party. A once in a decade event in China. Added to that of course will be the disruptions caused by the "storm of the century". And, if that was not enough, PMI data starts on Thursday. A quick snap shot of global growth starts. And earnings continue. As I say every week, what a week to look forward to.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment