More records in Jozi

"Rounding up the top ten are Standard Bank and Kumba Iron Ore. Whilst Standard Bank would be the company that derives most of its earnings locally, 92 percent as per the 2011 annual report, Kumba Iron Ore exports most of their product (37.1 Mt out of 41.3 Mt iron ore produced was exported, 68 percent of that to China), which is priced in Dollars. So that is the point that I am trying to make. Out of the top ten listed companies here in Jozi, only Standard Bank really could be considered a pure domestic company. But they have a fast growing business across the rest of our continent."

Jozi, Jozi 26o 12' 16" S, 28o 2' 44" E. Another Monday past, but another closing high for the Jozi all share. There are many people who cannot understand how that should be the case, especially in light of the recent strike action in South Africa. Surely, they observe, the job losses and poor relations between all parties is a negative in South Africa, and for the broader economy? The Reserve Bank is looking at lowering their growth targets, surely that must be very bad for the stock market? Well. This is not the case. Whilst the stocks don't all carry 100 percent weighting in the overall index, because many of these are watered down by the folks that put together the index, the biggest stocks are still huge relative to their market peers.

But hear me out, because there is a point to this. The top 15 companies listed on our exchange, out of 377 business listed, make up nearly 62 percent of all the value. The other 362 companies make up only 38 percent of the overall value. But listen in here, the top 9 companies listed here make up more than 50 percent of all the listed companies by market capitalisation. Phew. But here is the point that I am trying to make. The top six listed entities by market capitalisation (in this market, that is, BHP Billiton has two listings, plc and limited, we only follow the plc here) are 42 percent of the overall market cap. But of those 6, 5 have primary listings elsewhere. British American Tobacco, SABMiller, BHP Billiton plc and Anglo American plc all have primary listings in London, whilst Richemont has their primary listing in Zurich. Only MTN, in fifth place has their primary listing in South Africa. As per the 2011 Annual report, MTN derives 57 percent of their revenue from South Africa. And that has been decreasing over time. All the rest is "dollar" revenue, I guess.

In seventh place on the market cap ranking table is Sasol. Their "product" is priced in Dollars. Naspers is in eighth place, and we all know that TenCent makes up a large portion of the Naspers price. In fact, Naspers has a market cap of 221 billion Rands, TenCent has a market cap of 480 billion Hong Kong Dollars, Naspers own 34 percent of TenCent which equals 163.2 billion Hong Kong Dollars. One Hong Kong Dollar equals 1.1349 Rands, so that Naspers share in Rands is equal to 185 billion Rands. The rest of the business, Mail.ru, the whole of Multichoice, Allegro, Ricardo and all of the print media businesses are worth 36 billion Rands. Because I guess the market participants here are "scared" of a 35 times market valuation afforded to TenCent by the Hong Kong equity investors. Crazy.

Rounding up the top ten are Standard Bank and Kumba Iron Ore. Whilst Standard Bank would be the company that derives most of its earnings locally, 92 percent as per the 2011 annual report, Kumba Iron Ore exports most of their product (37.1 Mt out of 41.3 Mt iron ore produced was exported, 68 percent of that to China), which is priced in Dollars. So that is the point that I am trying to make. Out of the top ten listed companies here in Jozi, only Standard Bank really could be considered a pure domestic company. But they have a fast growing business across the rest of our continent. So for 53 percent of the market capitalisation of the JSE, only Standard Bank (who is moving forward) is an out and out domestic business. And that is why the economy and the market are not as connected as you might think. Do you think that I have explained this effectively? I hope so.

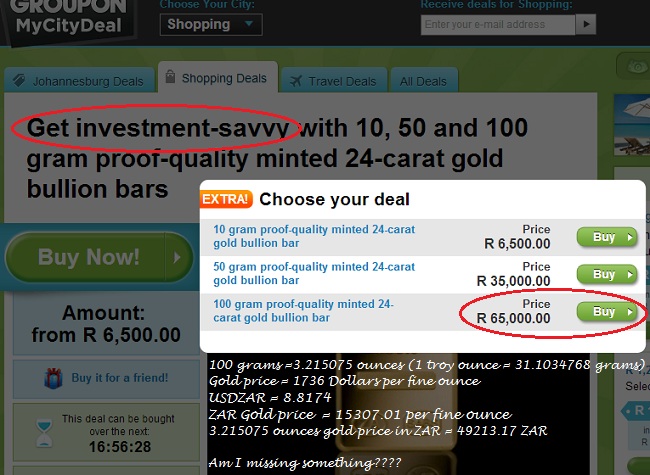

What the ....? I subscribe to the Jozi Groupon email daily, and have used it a couple of times, only a couple. But I look every day just to see what is out there. So today, there came a Groupon: Get investment-savvy with 10, 50 and 100 gram proof-quality minted 24-carat gold bullion bars. Yes, I thought, let me check this out with my anti gold as an investment obsession. Something did not quite stack up for me, once I had clicked on the headline link. 100 grams of gold for only 65,000 ZAR. That's all people! That's all.

1 troy ounce, as per the interwebs = 31.1034768 grams. US Dollar ($) / South African Rand (ZAR) = 1 USD = 8.8174 ZAR. And then 100 grams = 3.21507466 troy ounces. So, how many Rands, as per the market price, is 100 grams of gold worth? 49,213.17 ZAR. That is right sports lovers. You can get investment savvy and buy 100 grams of gold in Rands for 65,000 ZAR. Errr..... So I am guessing that you pay for the delivery which is a "great investment". I took a screen grab, and did the math on the image.

Who is savvy now? All I am going to say, is that if you want to own gold in Rands, you can buy it in the market, ticker GLD. Someone who holds the NewGold Exchange Traded Fund units is better off, both from a transparency point of view AND cost point of view. What are you going to do with a 100 grams of gold at home other than worry all the time that someone is going to steal it? Perhaps that is what you are paying the premium for, to stare at something shiny. A metal that has held man captive for centuries, no millennia. In Rand terms, the price of gold has been a massive investment since the launch of the ETF. Over five years GLD is up 189 percent, Harmony has gained 3.5 percent. Gold Fields is down 16.5 percent over five years. AngloGold Ashanti is lower by a percent and a half over five years. Over five years the Rand has weakened by 26 percent to the Dollar. The rest is the gold price.

We still prefer to be invested in companies. I would rather own Richemont than gold coins. Richemont sell jewellery and watches, and many other luxury items. Their dividend is paltry and the claiming back from the Swiss government is a pain, but at least they pay a dividend. If you get a one and a half percent yield from a stock, and reinvest it in that stock each and every year for the next twenty, you would have grown your investment by 30 percent. All I am saying is that gold has no yield, and a holding cost. There will always be a place for bullion, for some people, but like I said, I would prefer to own Richemont. A company that makes fine quality luxury goods, and sells them to wealthier folks. Who then own the watches and jewellery as an investment and heirloom, to pass down to their offspring.

Omnia released a trading update this morning: "Shareholders are advised that the Group's basic earnings per share and headline earnings per share for the 6 months ended 30 September 2012 are expected to be between 520 cents and 555 cents (based on a weighted average of 66.449 million ordinary shares in issue), an increase of between 50% and 60% on the prior year's published basic earnings per share and headline earnings per share of 346.8 cents (based on a weighted average of 66.322 million ordinary shares in issue)."

Whoa! And not surprisingly the share price is up 54 percent over the last twelve months, with the all time high reached in the middle of September, just over a month ago. Amazingly this is a business that had a rights issue not so long ago, not that this has too much to do with the numbers. That cash was earmarked for expansion, the building of a nitric acid and ammonium nitrate facility in Sasolburg was approved by the board in May of 2010. So you could argue that this was money well invested, not spent.

The second half of the year, the half coming traditionally is much better from a revenue point of view, but that makes sense in terms of the seasons, not so? But what now? The stock like I pointed out has had a magnificent run. The revenue and profits split as per the 2012 annual report for the three separate divisions are as follows: Mining, 3.051 billion ZAR revenue, 476 million ZAR in profits. Agriculture, 4.476 billion ZAR revenue, 323 million ZAR in profits. Lastly, Chemicals, 3.418 billion ZAR revenue, and only 86 million ZAR profits. I am guessing that you should only really then "worry" about the two biggest divisions, but that would be wrong. The nitric acid plant has only been in production since March of this year, and as far as production facilities look, it sure is swanky, and should add as much as 40 percent more capacity than the first plant. This also reduces costs in the fertilizer and explosives production facilities, as now Omnia has their own feedstock.

At the risk of sounding too bullish on commodity consumption, both soft and hard, I would think that Omnia is still an interesting proposition at these current levels. The price forward to March next year trades on a very undemanding multiple of 10.4 times. Relative to what is a tiny sub grouping of shares in their "sector" they have the most compelling fundamentals. It all does depend on continued demand from mining for explosives, that might have some way to go, but I suspect that the future of agriculture in Africa, that has an exceptionally bright future. The only question mark is whether or not there would be outlandish sized orders for fertilizer which follows a rapid rise in agricultural commodity prices, that might see too rapid a rise. But that does not sound like a "bad" thing.

Digest these links.

Excellent, as per the Nobel website yesterday: "The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2012 was awarded jointly to Alvin E. Roth and Lloyd S. Shapley 'for the theory of stable allocations and the practice of market design'" Lloyd Shapely is all of 89 years old and won a medal for bravery in the Second World War. Wow. That is truly amazing. You can check them out The Prize in Economic Sciences 2012. My only observation was that now they could afford a shave and a haircut. Stupid. If you have a spare 30 minutes (I didn't) check out the STABLE ALLOCATIONS AND THE PRACTICE OF MARKET DESIGN. And when citing this page, I am supposed to use this link too, to stay out of trouble: The Prize in Economic Sciences 2012 - Scientific Background. Excellent. Well done to those two, ra-ra!

The FT ran this story last evening: Spain prepares to make rescue request. There is a key paragraph in there, the third paragraph in which a senior Spanish Treasury official suggested that Spain would NOT make any request from the ESM. BUT, and this is a big but, Spain would satisfy all the conditions in order to get the credit line, if they need it. As we discussed in the office here, that is actually very clever. It is almost like waving a big stick at the "bond vigilantes", saying that if we need to use this, we will. So be careful. So it seems that conditionality is the key here and more important. Being in a position to accept funds in case of the worst case scenario. Now what? The WSJ has the same story, different angle, same conclusion: Spain Outlines Bailout Path.

Meanwhile in the WSJ daily piece: What's News: Business & Finance was a "I told you so" paragraph, but rather innocuous one at the same time: "Greek bond prices rose to their highest level since this year's debt restructuring as fading concerns over a euro breakup heartened buyers." Hah! Although the country is a long, long way away from the tipping point, this is surely progress. Lastly, Spain have JUST issued debt in an auction that exceeded expectations. And the German sentiment reading, although bad, was brighter than the reading before. See. Europe is fixing their problems slowly.

- Byron's beats

Over the last few months we have seen lots of negative data come through from the Chinese economy. Slow exports, low PMI and slowing GDP growth have all showed signs of a weakening economy. But remember that in July the Chinese central bank lowered the one year lending rate by 0.31% and the deposit rate by 0.25%. They also allowed banks to lend at 70% of the benchmark which was down from 80% previously and made loans more affordable for borrowers.

That was their internal reaction but let's be honest the biggest reason for the slowdown was Europe. If a European family could not afford that washing machine which was made in China because the bread winner lost his/her job then China would lose an export. This is why Chinese exports only grew 2.7% in August which for China's standards is a huge disappointment.

But a combination of local stimulus, a possible turn around in Europe and a US economy showing some good signs of long term growth has resulted in September data looking a lot more positive. This WSJ article titled China's Glass Is Half Full has pointed out some key data releases this month which could indicate the speed bump has been passed.

Growth in exports for September increased exceptionally from August to 9.9%. Lending figures also looked good. Lending figures were also positive. Total social finance, a central-bank measure of new bank loans, bond issuance and other forms of finance, expanded to 1.65 trillion yuan ($263.3 billion) in September, up from 1.24 trillion yuan in August. Medium- and long-term loans to business and corporate-bond issuance-used to fund investment-were strong.

Industrial output and investment data will only be released on Thursday but these should shed more light on a turn around. The article suggests that these numbers may be a little too late to have any effect on third quarter GDP figures so don't expect too much from that release.

Pending the news on Thursday this kind of article reminds me time and time again that you need to stick to your guns and focus on the long term picture. It may be hard at times when the data is looking negative to stick to your thesis. But I can honestly say that during the spate of negative data coming from China I always believed that there was no way China were going to experience a hard landing based on the dynamics of that economy. But let's not count our Chickens and wait for Thursday. Even if the data is not what I am looking for it won't change my mind, patience in these markets is priceless.

Crows nest. German economic sentiment beat expectations, which meant that the Euro crossed through the 1.30 to the Dollar again. There is some US inflationary data later, but for the time being I am excited to tell you that it is about earnings today!! JNJ, IBM, Intel and United Health and Coca-Cola all have results today. That is where the excitement is at. We are trading at another all time high today. The Rand is weaker.

Sasha Naryshkine and Byron Lotter

Follow Sasha and Byron on Twitter

011 022 5440

No comments:

Post a Comment