"FirstRand has a market cap of 291 billion Rand, most of the operations are here in South Africa, perhaps the two of them could be seen as the biggest out and out South African businesses, perhaps FirstRand even more so with around 90 percent of revenues derived from South Africa. The point is certainly worth making, our market is dominated by businesses that do not reflect the economy."

Golden eggs, magic beans, cinders and hair, giants and Englishmen, red hooded girls beware 10 in a row is good if you are getting your green number at Comrades, and you managed to do them consecutively, that is good, what is not good is when you have ten days of the market being down in a row. True story. It does not quite feel like it, possibly as a result of the quantum of the moves, they are not as severe as I have seen them in the past. September through October last year saw the ALSI lose nearly 5000 points, from our recent highs in April we are off around 3000 points. The last two months have been average for equities as a whole. I remember in May two years ago when the equities market locally had a similar slump, in terms of the number of points, obviously with the index being around 40 thousand points back then it felt worse.

So what is driving this sell off? Are valuations too demanding? Some folks will tell you that this is always the case, stocks are always too expensive and they are waiting for a pullback, please ring in the bell in both instances. The truth is that neither you nor I know, nor should we care too much about the shorter term moves. Still, that does not answer the question, what is causing this recent sell off? It is possibly a global sell off, related to two things, I think. One, the Greek issues are NOT going away. For more than just a while. Their debt issues are not insurmountable, it is seemingly a stalemate for now. I suspect that there is another 11th hour agreement in the works.

Secondly, the US economy has shown signs in the first quarter of more than just slowing, in fact the data points (which the Fed are watching) have been weak lately. Friday is the "jobs" number. The US Employment Situation is what the BLS (Bureau of Labor Statistics) calls it, the rest of the market knows it as the jobs report. And for better or for worse, it is the most watched, most anticipated and most traded around number in markets. So I am guessing that this Friday it will be no different, perhaps in light of recent worries (there is always something to worry about), the number might be more important than usual.

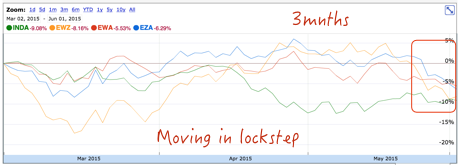

What I wanted to show in the next graphic however is that when there are a few "things" impacting on markets, then you could be forgiven for trying to find a local reason why the Rand is weaker (you know, the usual suspects) or why the local market is down. Here however is a combination of Dollar based ETF's that represent a few countries around the world. I have tried with my weak graphics skills to show that one gets sold off, all gets sold off.

The blue line, EZA is the South African iShares index, INDA is the green line, that is the iShares MSCI India ETF, the red line is iShares MSCI Australia, whilst EWZ, represented by the orange line is the iShares MSCI Brazil ETF. Brazil, Aussie, India and South Africa. All impacted by the same things, all impacted by exactly the same concerns that exist. It is absolutely no coincidence that a 3 month graph of the Dollar index (the basket against the major currencies worldwide) looks not too dissimilar to the inverted graph of the above, courtesy of MarketWatch:

The area I have circled explains it all. Wait, there is however more. As Paul pointed out however, the weakening Japanese Yen has juiced up the markets in Tokyo, the Nikkei 225 was up 12 in a row, until today. 12 days of up in a row, possibly all linked to the weaker Yen. Check it out from the same MarketWatch source, looks the same as the above graph, so actually, it has all got to do with the stronger Dollar:

So whilst we can identify, or try to identify, what is driving markets in the very short run, and that volatility is always going to be a part of investing, these are factors that we have absolutely no control over whatsoever. The Fed, the strength of the Dollar which equals weaker Rand and most other currencies. What to do? Don't panic mechanic, as my parents used to say to me. The last thing to do when equity markets go through a volatile patch is to be spooked. These happen from time to time, as we say over and over again, it matters what you own over a lengthy period of time. The more quality shares that you own (not too many however), the better the outcome over time. Keep calm. Carry on. Or as you were.

Following on from last week, when we had a look at the various company share registers that were mostly owned outside of South Africa, I got a reply from a friendly fellow at SABMiller, who informed me that the SABMiller London versus Johannesburg shareholder split was 83.9 percent London, 16.1 percent Johannesburg. How is that possible? SABMiller moved their primary listing to London in March 1999. All the deals along the way, Colombia's Bavaria (the Santo Domingo family became big shareholders then, 14 percent) in 2005. In 2002, earlier in the cycle of beer mega-deals, Altria (Philip Morris back then) became the biggest shareholder with the amalgamation of their Miller with SAB, hey presto, SABMiller. Altria owns 27 percent.

The question is, how did that happen? How, in 16 years, did all the shares end up in London? Deals! Again this stresses that this is not a South African company, of course the important part (as per an email to a journalist), worth sharing is the following. Her questions were simple, they asked whether or not the stock was expensive on a 23 multiple and why was it that the market was willing to pay so much. I share my answer:

We are not invested in the business at all.

Be careful of getting hung up on the multiple, sometimes businesses are expensive for a reason.

Remember that there is a very loose shareholder, not really in the inner circle so to speak, which is also the largest shareholder, Altria. They could do almost anything, in order to shore up some cash.

The reason why it is seen as an emerging market company is simple.

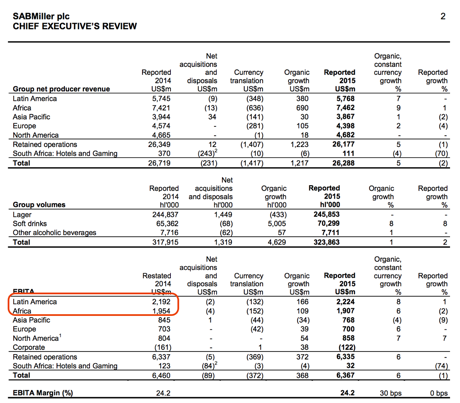

I have circled where the profits come from, Latam and Africa. See, it is an emerging market company!

OK. So there is our personal view, more importantly following on from the Friday message: Investors Paradise, we can now deduce South African ownership on the respective share registers:

British American Tobacco, 16.8 percent local ownership, 228 billion Rand of the 1.358 trillion Rand market cap.

SABMiller, as we have learnt, 16.1 percent local ownership, 174 billion Rand of the 1.081 trillion Rand market cap.

Naspers, that was the only company with a primary listing, as we discussed Friday, it is only listed here and is somewhat a proxy for Tencent and has a market cap of 764 billion Rand.

Glencore, I called the investor relations people and there were none available, I cannot think that it is too many shares in issue here, relative to London and Hong Kong, however. Liquidity here is only around 5 percent, we can go with that number, which translates through to 35 billion Rand.

Richemont, roughly 20 percent of the shares are held here in Johannesburg, about 110 billion Rand.

And then lastly, BHP Billiton, remembering that the local register is not all of the company, roughly 96 billion Rand owned by local shareholders.

Again, the point worth making is that the prices are not necessarily, if at all, set by the folks making investments here in South Africa. We are all held sway by the movements in Hong Kong (Glencore and Tencent), London (BATS, SABMiller, Glencore and BHP Billiton), as well as Zurich (Richemont) and Sydney (BHP Billiton). Glencore is listed in three places, as is BHP Billiton.

I guess then the only real totally African local stock, influenced by local factors could be MTN (market cap of 400 billion Rand), as we well know however it is closely linked to the movements in the oil prices as two of the big three countries by revenue, Nigeria and Iran, derive their export revenue from oil. FirstRand has a market cap of 291 billion Rand, most of the operations are here in South Africa, perhaps the two of them could be seen as the biggest out and out South African businesses, perhaps FirstRand even more so with around 90 percent of revenues derived from South Africa. The point is certainly worth making, our market is dominated by businesses that do not reflect the economy.

Linkfest, lap it up

This was via the Carpe Diem daily blog: Here's How Many Internet Users There Are. The number had grown from 738 million to 3.2 billion in 15 years, from 2000 to present. Africa, our continent, has only 20.7 percent of the population using the internet. Wonder how us Africans are going to consume more internet? Mobile, that is how. Stay long MTN and Vodacom.

How disruptive is Airbnb? I have used it, once. It is of course no different to using any other online booking platform, all you need is a credit card and away you go. I suppose you would not be surprised to hear then that Airbnb Is Approaching One Million Guests Per Night. Buy to rent may be replaced with buy to Airbnb.

Are you a restaurant snob? I mean, do you check the reviews and wonder if the foodies eat there? Maybe. One thing, food is more addictive than anything else. You have to eat in order to survive, it is that simple. Eating at the top 100 restaurants in the world, as per the voting by ... I am not sure, you figure it out: The World's 50 best restaurants. My only interest in this is that Cape Town restaurant The Test Kitchen clocked 28th place (well done), and Franschhoek's The Tasting Room, which came 88th (tie with a restaurant called Zuma in Dubai). Well done, culinary excellence all around. Of course this is subjective, don't you think?

How much would you pay to have lunch with Buffett? - Buffett Auction Draws $1 Million Bid, Exceeding 2014 Pace. It is a great way to raise money for charity. It also turned out to be a job interview for Ted Weschler a few years back.

This is not a new fact, what interests me though is how far out these forecasts are made - Charting Europe's demographic time bomb. "Today, there are around four working-age people for every pensioner aged 65 or older, but by 2060, there will be only two workers to support every senior.". This may come to fruition but I think we are more likely to see migration from developing countries to developed countries.

WhatsApp. We have an office group, it is both useful and entertaining. Here is a piece in which Microsoft director of office envisioning (yes, really) says: social media has already colonised your company. I suppose the beauty was and is that the app operates across all platforms and most phones, poor Blackberry was blindsided by this.

And they all lived happily ever after. Make that 11 in a row. We are going to have to do a lot in order to make sure that this does not happen again today, the weaker local unit is still as a result of a weak Euro. And the ongoing talks between the Greeks, which seem to have broken down somewhat. There is progress, whatever that means. I stand by the 11th hour solution.

Sent to you by the Vestacters, Sasha, Michael, Byron and Paul.

Follow Sasha, Byron and Michael on Twitter

087 985 0939

No comments:

Post a Comment