"There is a reason why the company trades where it does, Mr. Market always knows something. The company guided for the full year ahead, sales growth of around 6 percent in Dollar terms, earnings per share is expected to be 5.50 to 5.70, which means that earnings are growing by 45 percent plus. And forward, the stock trades in the region of 17 to 18 times earnings, which is about where the market is currently trading overall. So the stock price is bang on, spot on, relative to their growth prospects, at the moment."

To market to market to buy a fat pig. Oh no, what happened? The rally was scuppered by the sinking oil price once again, worries around global growth rates persist again. Should we be worried about the big picture? I guess we should always take them into consideration, of course the companies that we buy and hold for clients are a lot more important in the bigger picture, equally if those same said companies are selling into a softer environment, that is going to have a negative outcome for them. Sales can't consistently be higher in an environment where Joe Consumer is scratching around. Having said all of that however, I stand by my outlook for an improving European economy to capture the imagination this year. I read on the BusinessInsider yesterday that the investment team at Charles Schwab had Japanese and European markets as their best ideas for the year. Sadly no emerging markets, sigh.

With a giant sell South African assets button being pushed by someone yesterday, the market certainly came in for some heat. In fairness, whilst sometimes we think it has something to do with us, looking across at the other markets of the world we can quickly tell that is was pretty much a global sell off. The FTSE down over two and one quarter of a percent, the DAX over in Frankfurt fell 1.8 percent, the CAC in Paris was down nearly two and a half percent. So I guess it should hardly be surprising that our market was down 2 percent on the day, led lower mostly by Resource and Financial stocks, both those indices down 4.09 and 3.94 percent respectively. Most of our selling accelerated downwards from around 10am local time, that is when all of the European markets open. The only stocks that showed any gains on the day were the companies that had a Rand hedge bias, SABMiller, AB InBev, Reinet, British American Tobacco, Capital and Counties and Intu. All those stocks have primary listings elsewhere.

Over the seas and far away in New York, New York, stocks sank all the way into the close of the session, the nerds of NASDAQ sank two and one quarter of a percent, both the broader market S&P 500 and the Dow Jones Industrial Average lost around 1.8 percent on the day. Google, I mean Alphabet, added only 1.68 percent on the day after their particularly sparkling results. The market cap, for those of you who are checking, is 523 billion Dollars. Apple, at last check is 534 billion Dollars. And to think that yesterday Google was the largest company in the world. I can't say that I have seen a headline that says that Apple is now the number one company by market capitalisation in the world. No? Yes? Anyone?

Stocks across Asia are also feeling the heat, the Nikkei is getting thrashed, down 3.25 percent, there and thereabouts as we speak. Chinese markets are down too, the Hang Sang is down 2.7 percent, the Shanghai market is down over a percent. We should start a whole lot lower today, again I am afraid. Knock, knock, knocking at the door, bargains are beginning to appear again on our screens. Line it all up!

Company corner

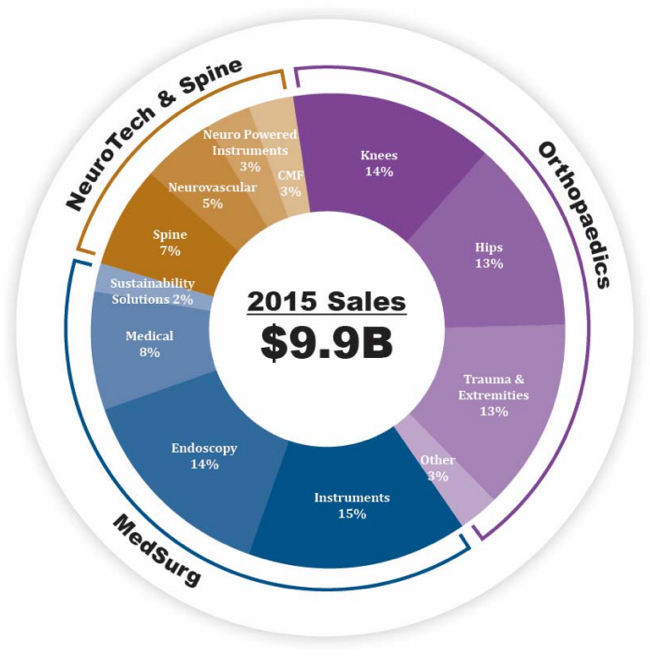

Stryker, the medical devices business, reported numbers last week, and guided for the year ahead -> 2015 Results and 2016 Outlook. As you can see at face value, the company had a tough year, still, it was definitely acceptable. Total sales for the year, net sales, nearly topped the 10 billion mark, 9.9 billion Dollars, net earnings of 1.4 billion Dollars was achieved. On an earnings per share basis the company chugged out 3.78 Dollars, at 99.30 Dollars where the stock closed last night it trades on a historical multiple of 26.2 times, not cheap by any stretch of the imagination.

There is a reason why the company trades where it does, Mr. Market always knows something. The company guided for the full year ahead, sales growth of around 6 percent in Dollar terms, earnings per share is expected to be 5.50 to 5.70, which means that earnings are growing by 45 percent plus. And forward, the stock trades in the region of 17 to 18 times earnings, which is about where the market is currently trading overall. So the stock price is bang on, spot on, relative to their growth prospects, at the moment.

The company has three defined divisions, their biggest from a sales perspective is their Orthopaedics division, then Medsurg and lastly a more specialised division, NeuroTech and Spine. A JP Morgan medical conference presentation from their investor relations website breaks it down perfectly, a picture tells you everything you need to know:

The future looks exceptionally good for a business of this nature. Technology advances are going to work exceptionally well alongside a business of this nature. The company talks of advancing 3D printing of knees, revision cones as well as newer spine therapies. A quick browse through the orthopaedics product catalogue on the website -> Stryker Orthopaedics, gives you a good reminder that the future is here already.

The growth will continue to be via specialty acquisitions, the integration of Mako surgical is now complete (deal done in December 2013), don't confuse this with another purchase of Muka Metal, a maker of specialised hospital beds in Turkey. The company announced a newer purchase at the beginning of the week, they are buying a privately held business called Sage for 2.775 billion Dollars. As per the presentation, Sage "develops, manufactures and distributes disposable products targeted at reducing "Never Events," primarily in the ICU and MedSurg hospital unit setting".

"Never events" is a relatively new term, introduced by a MD by the name of Ken Kizer, it refers to procedures on the wrong body part, or on the wrong patient even. Here the NHS lists their definitions and guidelines for Never Events. It is a pretty smart acquisition all round and complimentary business, that adds just over 4 percent to total sales.

And almost all of the Sage business is inside of the US, only 5 percent outside, which means that there is more room for growth. These products are all designed to significantly reduce hospital acquired conditions, as well as improve the healthcare workers safety. Plus Sage is currently number one in a 1.8 billion Dollar market. As Stryker point out, 30 billion Dollars is spent annually in the US to treat the conditions that Sage can prevent, there are hospitals, patients, healthcare workers and medical insurance companies all on the same page here as far as priorities are concerned.

Growth will also come via pushing the business internationally, the sales split last year was 71 percent US and the rest being international sales. There is strong sales momentum in Europe, that recovery story should continue. Whilst this may not seem like the most exciting business at face value, their products are pushing medical science boundaries to improve the lives of many. And whilst society ages and is in desperate need for new knees, hips, as well as careful spinal products, it also improves the quality of life of all of us. To give someone the gift of less pain is worth more than the money shelled out, relative of course. As the world gets richer, so more of these products and procedures will become everyday and commonplace.

Whilst I don't see a runaway share price from here, I do think that this is one of the best business in this space globally, from the research that we have done at Vestact. We remain conviction buy, most especially if the stock sags from here. Remain patient (excuse the pun), lie in waiting, this company will certainly reward you in the long run.

Linkfest, lap it up

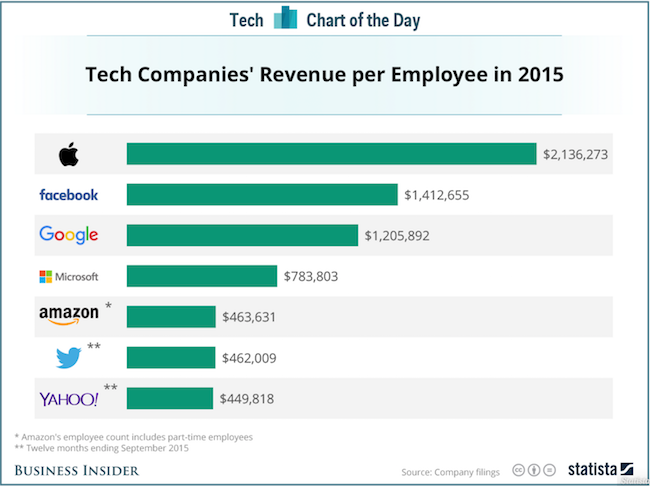

Tech companies have huge margins because once the IT infrastructure is in place and those fixed costs are covered, every new customer adds very little variable cost - Here's how much each employee at a big tech company like Apple or Facebook is worth. The graph below highlights why people in Silicon Valley get paid so much and why tech companies have so much cash sitting on their balance sheets.

One way to keep Uber drivers happy is to keep passengers happy and out of the hair of the driver - Can a children's toy stop drunken Uber passengers from attacking their drivers?

Ben Carlson took a look at how dividends have faired during market pull backs. Absolute dividend payouts don't seem to drop as much as the stock market probably because when people sell stocks during a panic they sell at any cost. The underlying business is still solid so the dividend is safe but the stock multiple is a lot lower - The Incredible Growing Dividend. A bigger story though is how much growth there has been in company dividends.

This is for laughs, kicks and giggles. I saw this via a tweet from Wu Tang Financial this morning, that account is a hoot. Hump-day fun with numbers.

Home again, home again, jiggety-jog. Stocks are not going to enjoy a good day today, it is going to be more signs of selling. There is of course some employment data out today, in the form of the ADP data, that is the precursor to the non-farm payrolls on Friday. At least that we have to look forward to. And the cricket today! That is always fun.

Sent to you by Sasha and Michael on behalf of team Vestact.

Follow Sasha, Michael, Byron, Bright and Paul on Twitter

078 533 1063

No comments:

Post a Comment