To market to market to buy a fat pig. One thing that I was reminded of while writing about Famous Brands, is that business is never easy. I have never read a set of results from a company, where they said 'things were easy, all we had to do was show up and we made money'. Generally, at least one division or region is struggling because of a tough operating environment.

In Famous Brands's case, their primary operations are in South Africa where consumer spending is down due to a lack of growth. Their other significant operating region is the UK, where things are more stable but thanks to Brexit, growth is also down. Moving along to their Rest of Africa (ROA) division, growth numbers look healthy but given lack of economic diversification, growth is volatile. On top of that, operating in the ROA can be challenging because of the struggle of getting capital in and out of respective regions. Then things like electricity, fuel and fresh produce are not always guaranteed.

Out of all the regions that they operate in, the UK is probably the 'easiest', in terms of a stable country with a wealthy customer base. Due to business being easier, there is more competition and their margins are razor thin. ROA, on the other hand, has less competition, meaning there are excellent thick and juicy margins to compensate investors for the increased risk. As the saying goes, 'if it were easy everyone would be doing it', and if everyone is doing it, there is no money to be made.

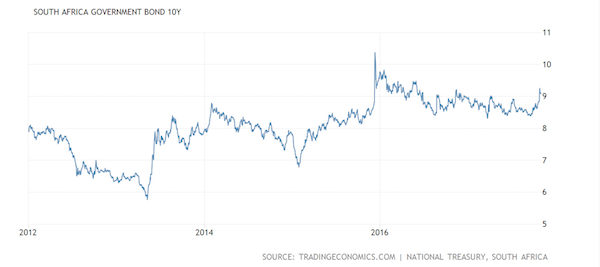

Market Scorecard. As expected the Fed left the US interest rate unchanged, and basically said if things stay on track, they should raise rates in December. The Dow was up 0.25%, the S&P 500 was up 0.16%, the Nasdaq was down 0.17% and the All-share was up 0.91%. Have a look at the interest rate on our 10Y Government bond; you can clearly see when 'Nenegate' happened. As it stands, we are still at better levels than we were for most of 2016. I found the graph at Trading Economics; in my opinion the best place to find any economic data that you may need.

Found at South Africa Government Bond 10Y

Found at South Africa Government Bond 10Y

Company corner

Michael's Musings

On Monday Famous Brands released their 6-month results, which we already knew weren't going to be pretty reading. Year to date the stock is down 34%, reflecting lower consumer spend locally and the struggles they have had with their GBK acquisition in the UK.

The purchase of GBK has made a significant change to the companies profile. The first impact has been on their gearing, the balance sheet went from having no gearing and debt, to having R2.9 billion in debt. Having some gearing is arguably a good thing, when management doesn't have debt on the books, analysts start to criticise saying the company has a 'lazy balance sheet'. Famous Brands still has a strong balance sheet but to get debt down to a level that management feel more comfortable with, they have suspended the dividend until at least next year. In years gone by, one of the reasons for buying Famous Brands was for their yield.

Over the last few years, their operating margins have steadily been falling from around 20% to the last period's 11.9%. The reason for their falling margins is mostly due to top line growth coming from low margin divisions. Over the last few years they have been growing the supply chain part of the business, where logistics has minute margins and high volume. The purchase of GBK put further pressure on margins due to margins in the developed world being lower than South Africa in general.

The biggest problem currently facing the group is foot traffic, over the last 6-months there was a 16% drop in foot traffic to their Casual Dining and Quick service offerings. The rise of UberEats and similar delivery services is a game changer for the industry. Customers are increasingly opting for the easier option of having food come to them instead of having to go to the outlet, how management handle this change will either make or break the company.

Their UK division has had a rough time, in September they closed the last Steers store and GBK made a GBP 872 000 loss. Management expects GBK to swing into profit during the next financial year.

An exciting launch next year is their Word of Mouth division, which will be launching 'Frozen for you' in early 2018; it will be home meal replacements, sold in store and online. Think Woolies food blended with UberEats. If they can get the value for money and quality/ healthy mix right, this division could be huge in the future.

In the short term, the share price will probably be volatile as management tries to turn around GBK and as the RSA consumer braces for the potential of a credit rating downgrade. There is no doubting the quality of their brands and the excellent job management have done in building a vertically integrated company. As a shareholder though you will have to ride through these bumps.

Linkfest, lap it up

One thing, from Paul

The most expensive commercial real estate transaction in history just closed in Hong Kong.

The seller was Li Ka-shing, Hong Kong's wealthiest man. The building is The Center tower, Hong Kong's fifth-tallest building with 73 storeys. The price was HK$40.2 billion (US$5.15 billion).

Interestingly, the controlling shareholder of the buying consortium is Beijing-based China Energy Reserve & Chemicals Group.

The slow assimilation of Hong Kong by mainland China continues - Li Ka-shing sells The Center in US$5.15 billion record deal to trim his flagship's Hong Kong assets

Home again, home again, jiggety-jog. Asian markets are mixed this morning, and the All-share has opened in the red; still above the 59 000 mark though. The Rand strengthened over night with a '13' in front of it when compared to the USD. Later today we should hear who the next Fed chair will be and a more detailed look at the Trump Tax plan. Facebook's numbers last night showed huge growth again! Tonight we have full year figures from Apple and 2Q numbers from Alibaba, exciting times.

Sent to you by Team Vestact.

Follow Michael, Byron, Bright and Paul on Twitter

078 533 1063

No comments:

Post a Comment